Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

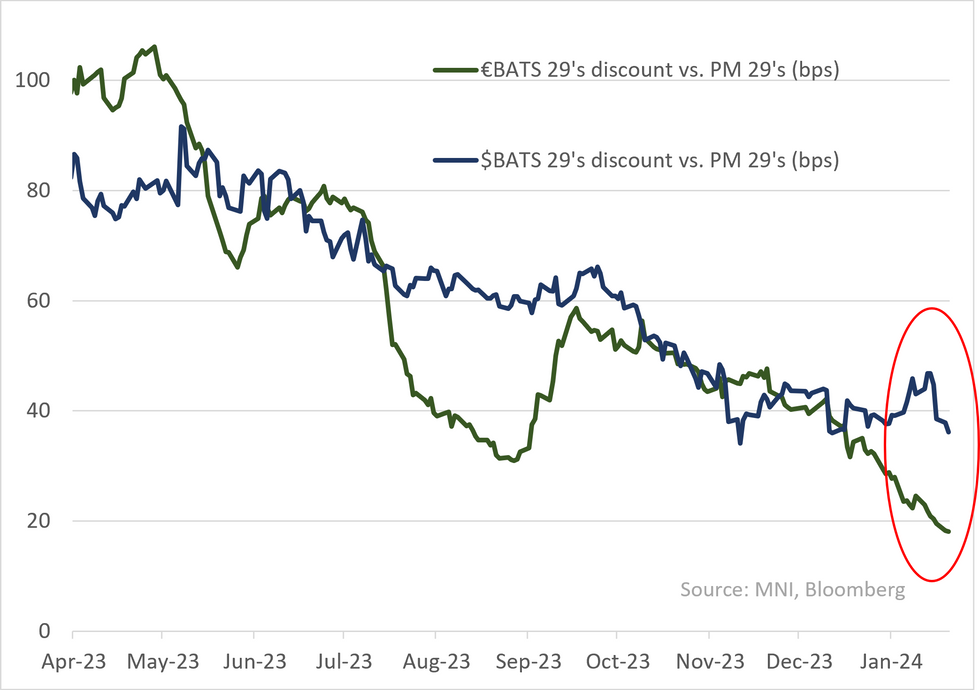

BAT's $1.7b 7 & 10yr deal saw strong demand; books covered 5.8-5.9* & with high single to low double digit NICs - that's in stark contrast to Philip Morris' Friday deal that came with double digit NIC's & books only covered 2.7*. We see this as a $ specific dynamic and still cautious on tightness in €BAT.

* $BAT curve still gives +50bps on spread pickup vs. $PM - In line with that yest's deal priced +38/+33 over PM's 7/10yr from Friday (rates another +5 for yield investors). Again swapping to Euro its the local/€BAT curve that screens tight.

* BAT running its healthiest BS in years with a outlook upgrade (to stable) yesterday morning from S&P (largely retrospective) & management is (still) guiding to deleveraging - all likely reassurance for the investors to come in for the spread pickup (vs. PM & index). The optimist outlook (particularly in €BAT) isn't shared by equity holders who are (by nature) more forward looking - BAT trades at forward P/E of 6.5* (down from ~10* in mid '22 & vs. PM at 13*) despite a trailing dividend yield of ~9.5% (dividends have been unaffected).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.