Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

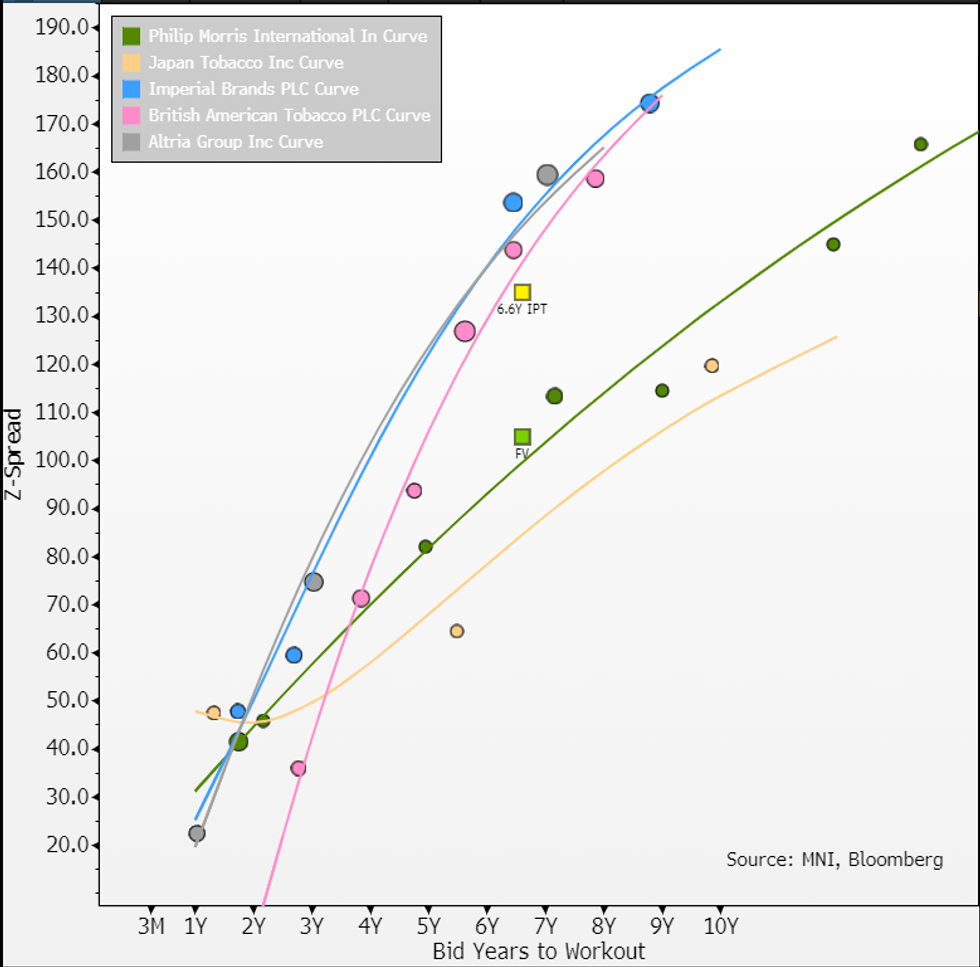

IPT +135 vs. FV +105, preferred curve remains BAT

- This is a 6.6Y (that's been rounded down). 7-month longer August line trades at Z+113/€84, our FV is 8bps inside it. For comparison BAT gives ~12bps roll-down here.

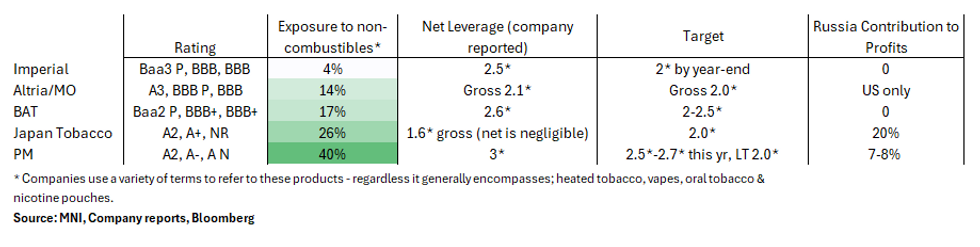

- PM has ~no US exposure & was former international arm of Altria that was spun-off in 2008. It records 5% revenues in Americas but includes Argentina & Mexico. Russia is 7-8% of EPS.

- It has the highest expected near term growth (FY/CY24 at +4.8% in net revenues & +6.6% in adj. operating income) - part of that is from its high exposure to higher growth non-combustibles (below).

- Our preferred curve remains BAT in this tenor on better carry & roll balanced with good geographical diversification & reasonable non-combustibles exposure. New BAT32s which we had a screen cheap on has done poorly; 40bp loss on +19bps carry & -59bps spread return - latter saw secondary curve reprice wider.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok