Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China's official PMI prints for September presented, in aggregate, a softer backdrop. Encouragingly, the manufacturing PMI moved back into expansion territory, albeit just at 50.1 (49.7 expected). However, the Caixin manufacturing PMI slipped deeper into contraction territory at 48.1, well below 49.5 expected. The non-manufacturing PMI (official) fell more than expected as well to 50.6 (52.4 forecast)

- The detail showed output and new orders rising for the manufacturing PMI, but employment only just edged higher to 49.0. New export orders were also down to 47.0, but this remains above earlier lows (41.6 in April).

- The weakness in the Caixin MI still suggests headwinds for the SME sector. The Chengdu lockdown likely weighed on this space through the month

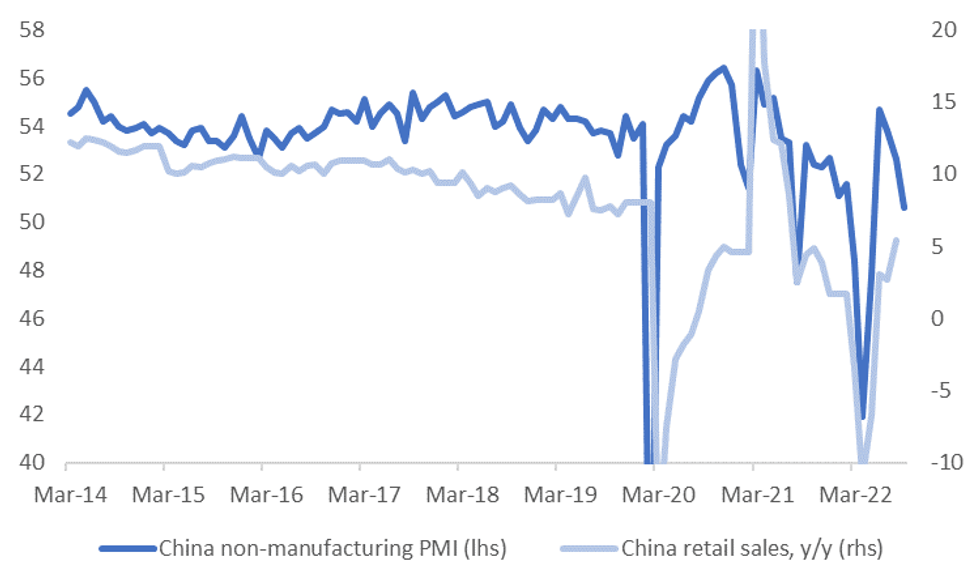

- The non-manufacturing PMI was always at risk of dipping given these Covid related headwinds in September. The chart below plots the headline reading against retail sales y/y.

- The detail was fairly soft in the non-manufacturing PMI, with new orders dipping to 43.1 (from 49.8 last month).

- With Covid cases coming down, there will be hope that conditions improve in October. Still, these updates may still concerns around near term growth momentum, particularly in the services/SME side of th economy.

Fig 1: China Non-Manufacturing PMI Versus Retail Sales Y/Y

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok