Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

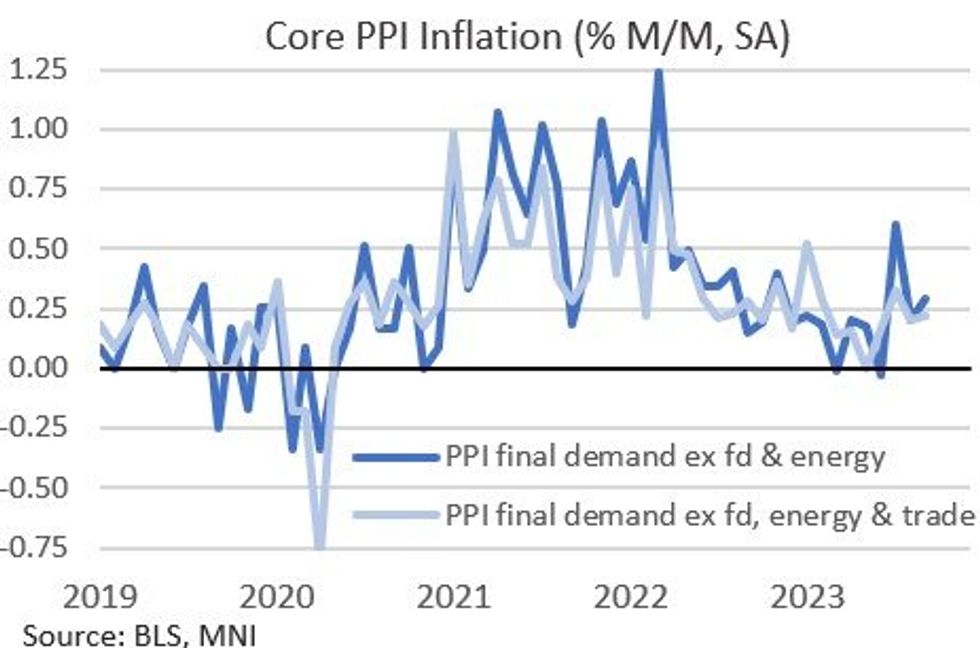

A higher-than-expected September PPI contained details that look less inflationary from a core perspective as we head to Thursday's CPI:

- The 0.5% M/M rise was higher than the 0.3% estimate (+0.7% prior), with ex-food and energy +0.3% vs 0.2% expected (+0.2% prior). Ex-food, energy, and trade services printed 0.2% M/M for the 2nd consecutive month (upon revision from 0.3% for August).

- Most of the increase in goods can largely be discounted from a core PCE / CPI perspective - 3/4 of the increase is due to the rise in energy prices (which pulled back sharply from 10.3% in Aug) as expected to be mirrored in the CPI release tomorrow. The jump in goods to a 10-month high +0.9% M/M was more concerning in this regard.

- Final demand services were up 0.3%, but the BLS notes that a major factor was a 13.9% jump in the index for "deposit services" (which had been negative the prior 2 months) - there's no explanation of this in the release but it's imputed from interest rate spreads.

- Looking at the PCE categories. Airline passenger services (which are used in PCE as airfares, and not the CPI reading out tomorrow) fell by the most since April, -2.1% M/M.

- Health care services ticked a little higher unrounded but were steady rounded at 0.1% M/M; health and medical insurance prices pulled back sharply to 0.2% from 0.5% prior.

- Insurance costs overall though pulled back to 0.2% M/M from 0.3% prior; auto insurance costs notably ticked higher.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok