Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

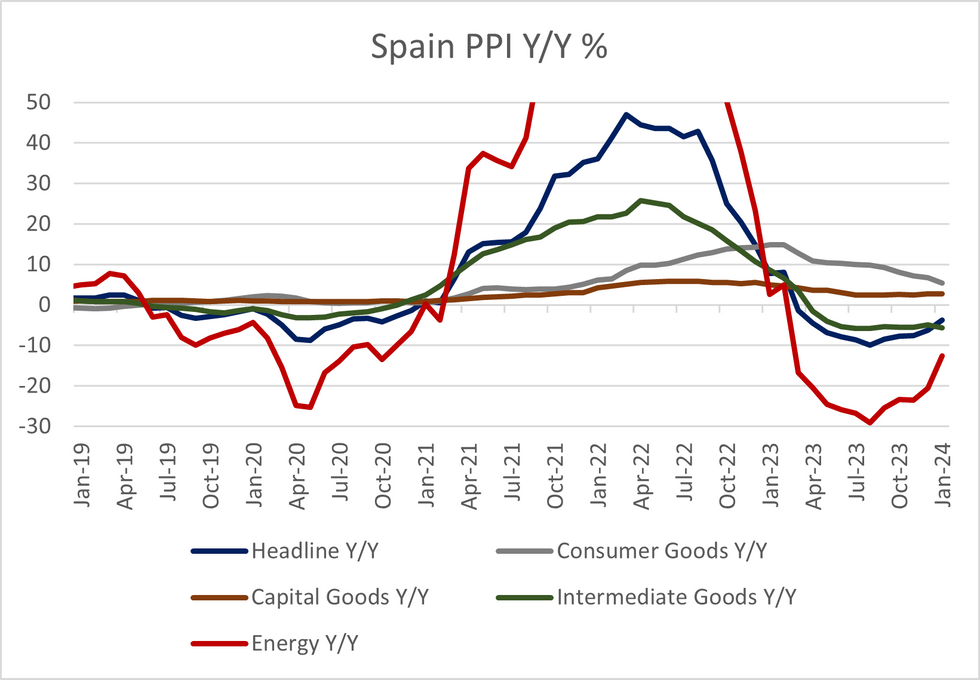

While still in Y/Y deflation, Spanish headline PPI reached its highest level since April '23, as the downward impact of energy base effects continues to fade. However, the other major sub-components showed continued disinflationary progress - an encouraging sign for the core goods outlook ahead of Thursday's February CPI flash release.

- January headline PPI was -3.8% Y/Y vs -6.3% prior. There was no consensus for the print.

- At a component level, energy PPI remained in deflation, but the -12.6% Y/Y was the highest since February '23 (vs -20.6% in December).

- However, we suspect that energy prices should continue falling Y/Y for several months yet, since the energy PPI index peak was seen in August 2022 (vs Italy who saw the peak in December 2022, for example).

- A reminder that Spanish flash CPI for February will be released on Thursday, with early consensus looking for a deceleration in CPI and HICP Y/Y inflation vs January (CPI: 2.8% Y/Y vs 3.4% prior; core CPI: 3.3% Y/Y (vs 3.6% prior); HICP: 2.8% Y/Y vs 3.5% prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok