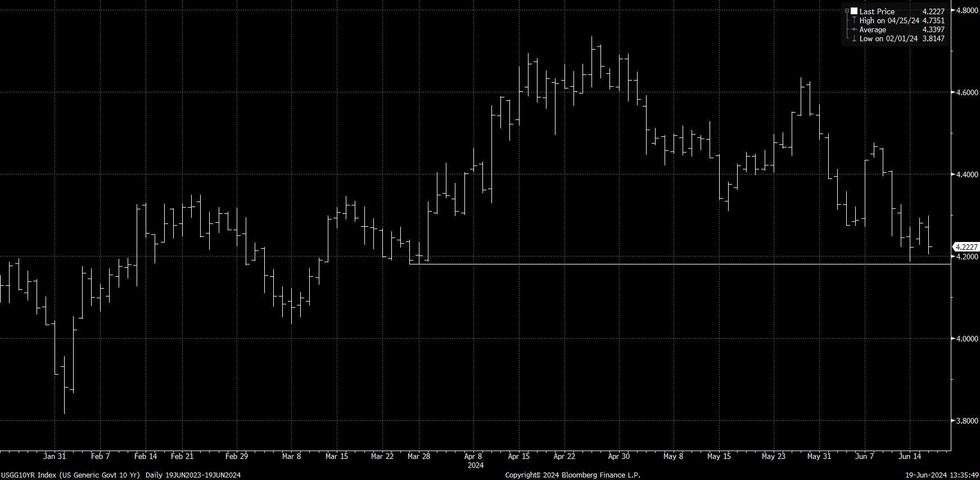

US TSYS

While cash Tsys are closed for the US holiday, the modest downtick in futures is set to leave the multi-week ranges in yields intact at the Asia cash open.

- Ultimately, the recent mix of Fedspeak, updated dot plot and general direction of travel for data has embedded the higher-for-longer rates mantra, albeit with some contained bouts of volatility around recent tier 1 data releases.

- May’s PCE data (Jun 28) provides the next meaningful inflation input, with CPI & PPI already biasing sell-side estimates lower.

- The early BBG survey medians point to +2.6% Y/Y for both headline PCE (vs. +2.7% prior) and core PCE (vs. +2.8% prior). While this is still above the Fed’s inflation target, Chair Powell previously noted that “if you're at 2.6-2.7%, that's a really good place to be.” This suggests that a run of inflation releases around those sort of levels could give the Fed greater confidence to actively consider reducing rates.

Fig. 1: U.S. 10-Year Tsy Yield (%)

172 words