Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

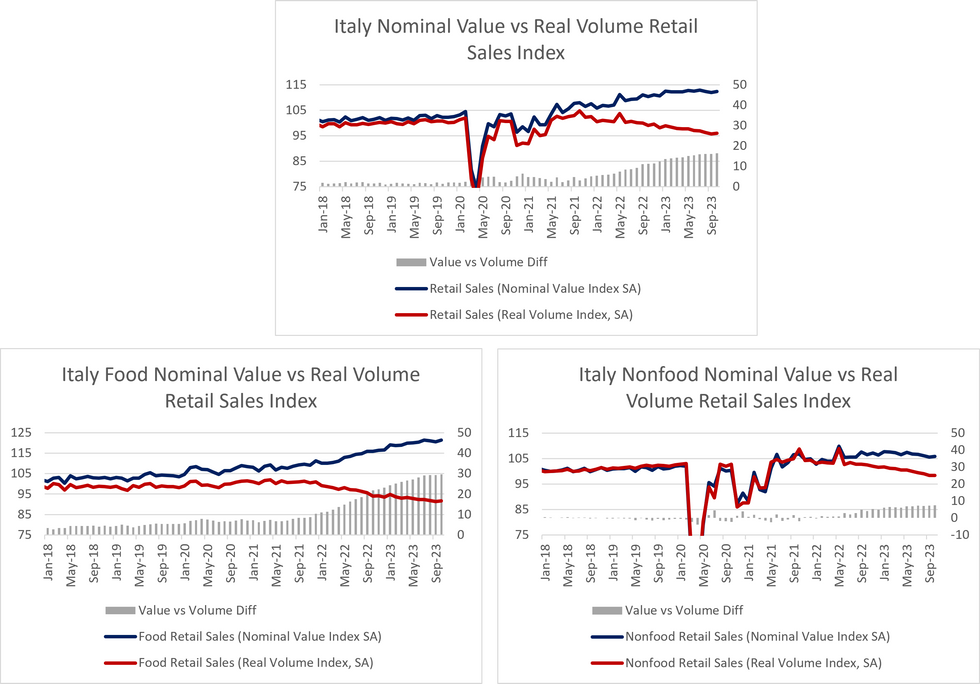

Italian October retail sales ended two months of negative SA monthly prints to rise +0.4% M/M (vs -0.1% cons; -0.3% prior) in nominal value terms. Despite this, retail sales continue to display stagflationary undertones, which may be feeding through to industrial production figures in the case of durable goods.

- Food products saw a larger monthly improvement than non-food counterparts, but continue to contribute most to inflationary pressures (shown by the difference in the value vs volume indices). This trend has been corroborated in recent CPI data.

- On an annual basis, sales rose +0.3% Y/Y in value terms (vs +1.2% Y/Y prior). Food products saw a +3.5% Y/Y rise (vs +5.3% prior) while non-food products fell -2.0% Y/Y (vs -2.0% prior).

- Within the non-food products basket, the largest Y/Y downside was seen in electric household appliances, audio-video equipment (-5.3%) and clothing (-5.0%), while cosmetic and toilet articles sales rose +3.1% Y/Y.

- Industrial production data for October was also released today, coming in at -1.1% Y/Y (vs -2.0% prior, WDA) and -0.2% M/M (vs 0.1% prior, SA). Consumer and intermediate goods showed negative Y/Y prints for the 9th consecutive month each, while capital and energy goods had positive annual rates.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok