Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

IDR

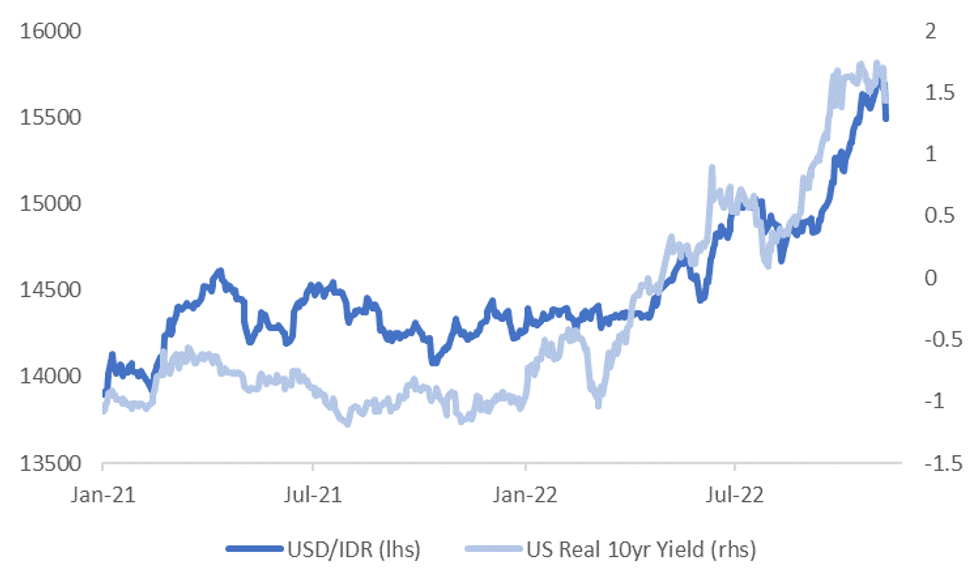

Spot USD/IDR is down nearly 1.30% from yesterday's closing levels, last tracking just above 15,500. The IDR is playing some catch up with overnight moves in the USD and the sharp pull back in US real yields following the CPI miss. The first chart below plots USD/IDR against the UST real 10yr yield.

- Post-CPI reaction allowed Indonesia's 5-Year CDS premium (one of the measures of rupiah stability watched by Bank Indonesia) to tighten to a fresh cyclical low near its 200-day MA.

- Of course, it remains to been seen how much further US yield momentum pulls back. Further downside should benefit the IDR based off current correlations.

- It's also noteworthy USD/IDR is still some distance above its simple 50-day MA (15,300), even with today's correction lower. A number of other USD/Asia pairs have already comfortably breached this support level.

Fig 1: USD/IDR and US 10yr Real Yield

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

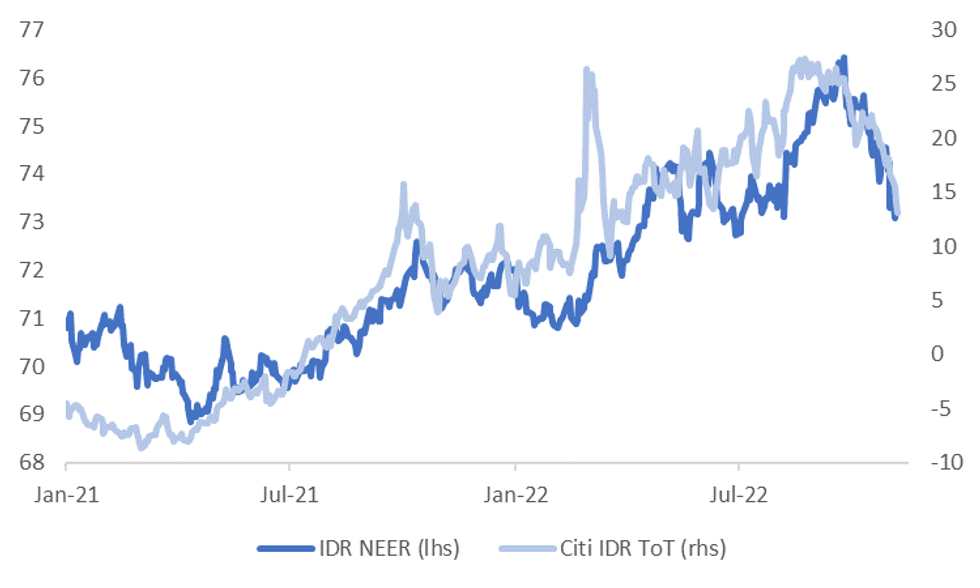

- Commodity price dynamics are still presenting a less favorable backdrop for IDR though. The second chart below overlays the J.P. Morgan IDR NEER versus the Citi IDR ToT proxy. Indonesia's status as a major commodity exporter has become a liability as the pass-through from deteriorating global growth prospects to the commodity markets became evident.

Fig 2: J.P. Morgan IDR NEER Versus Citi Terms Of Trade Proxy

Source: J.P. Morgan/Citi/MNI - Market News/Bloomberg

Source: J.P. Morgan/Citi/MNI - Market News/Bloomberg

- On a daily basis, however, the aggregate BBG Commodity Index is sligtly higher, consolidating yesterday's 1.25% advance. Palm oil futures trade MYR79/MT higher, albeit Indonesia's decision to lift its CPO reference price may undermine the attractiveness of Indonesian crude.

- With spot USD/IDR trading -176 figs at IDR15,516, bears set their sights on the 50-DMA, while bulls look to a rebound towards Nov 4 high of IDR15,750. USD/IDR 1-month NDF last -23 figs at IDR15,501, with bears keeping an eye on the 50-DMA at IDR15,320 and bulls targeting Nov 3 high of IDR15,838.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok