Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

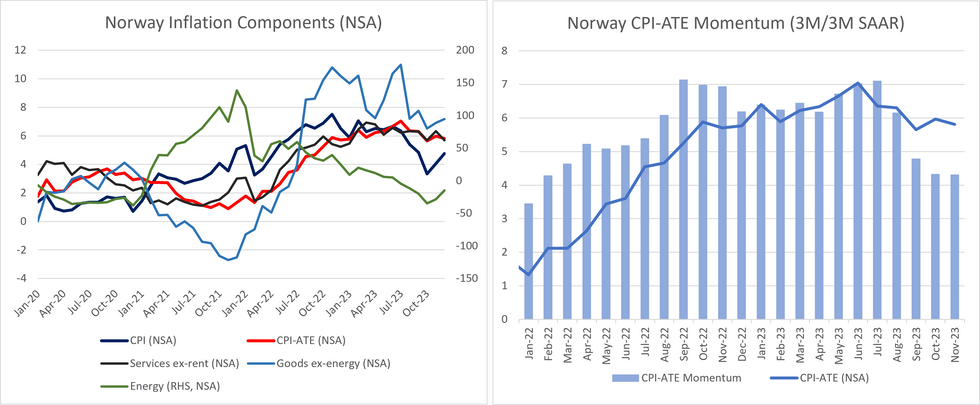

MNI's core inflation momentum indicator was broadly unchanged in November, with 3M/3M SAAR CPI-ATE inflation printing at +4.30% (vs +4.32% prior and +4.78% in September). This follows three successive declines and today's marginal decline signals a continued slowdown in trend underlying inflation pressures - a pre-requisite for the Norges Bank to hold rates according to their November policy guidance.

- In M/M SA terms, CPI-ATE rose +0.31% M/M, meaning it still tracks at a >2% annualised rate, but is well below the +0.71% M/M print seen in October.

- Component level data shows a softening in services ex-rent inflation to +5.7% Y/Y (vs +6.3% prior). While goods ex-energy rose to 7.2% Y/Y (vs +6.9% prior), this was due to the uptick in food prices seen in the latest month. Rents were a touch higher at 4.4% Y/Y (vs 4.3% prior), while energy became less negative at -15.0% Y/Y (vs -28.3% prior).

- The Q4 Regional Network survey in Norway did not signal a renewed uptick in wage pressures across sectors, which will be most relevant for the services sector, and should indicate continued softening of inflation pressures ahead. On the goods side, declining output expectations on the back of a weaker demand outlook should also help core goods soften in the coming months too.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok