Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

While the monthly and annual figures in the December CPI report were softer than expected, the seasonally adjusted series indicated relatively firmer price pressures. SA CPI rose +0.46% M/M (vs +0.61% prior) while SA CPI-ATE rose +0.31% M/M for the second consecutive month. Both run-rates are above the Norges Bank's 2% target when annualised.

- This suggests that the Norges Bank will be in no rush at the upcoming meeting to alter its December guidance, which notes the policy rate "will likely be kept at 4.5% for some time ahead".

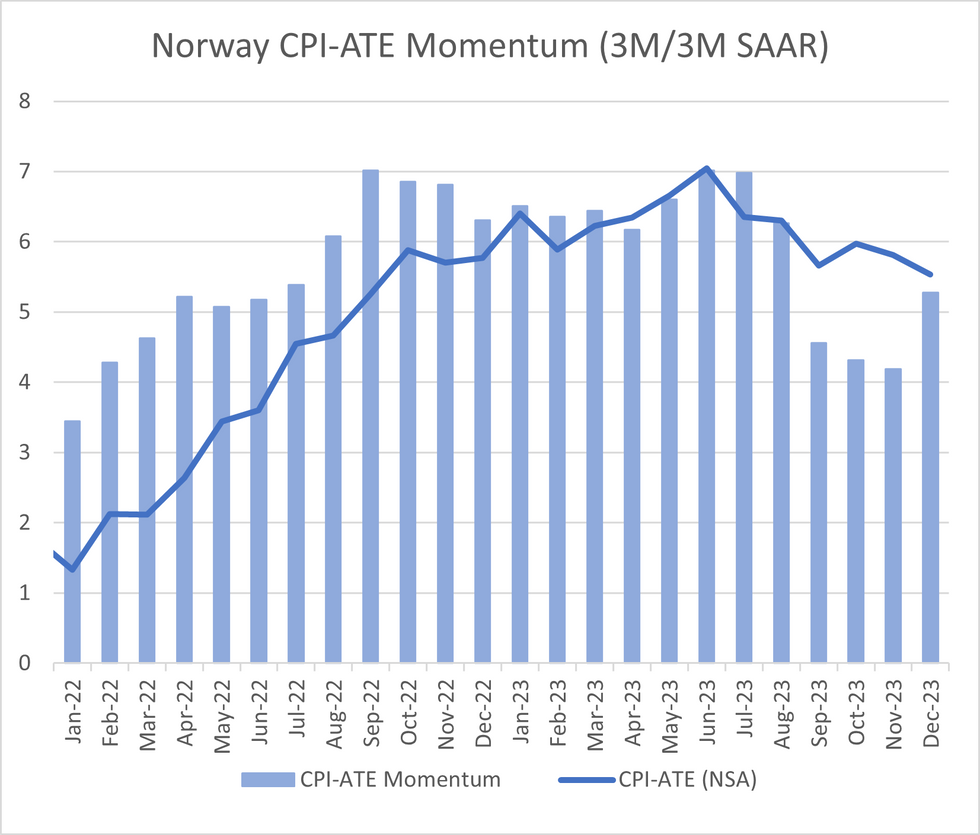

- As a result of the bounce back in energy prices over October and November (+11.3% M/M NSA and +17.4% M/M NSA respectively), headline CPI momentum, calculated as a 3m/3m saar rose to +5.23% (vs +1.86% prior, the highest level since July 2023). CPI-ATE momentum also accelerated to +5.27% 3m/3m saar (vs +4.19% prior).

- Rounding off the main sub-categories of the report (in NSA terms), services ex-rent decelerated to +5.1% Y/Y NSA (vs +5.68% prior) but were flat on the month. Core goods fell -0.8% M/M NSA in December, but softened a touch on an annual basis to +7.1% Y/Y NSA (vs +7.2%). Rents rose +0.2% M/M for the second month in a row, with the annual rate rising to +4.6% Y/Y NSA (vs +4.4% prior)

- Energy prices fell -9.8% Y/Y NSA (vs -15.1% prior), but fell -1.1% M/M NSA.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok