Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

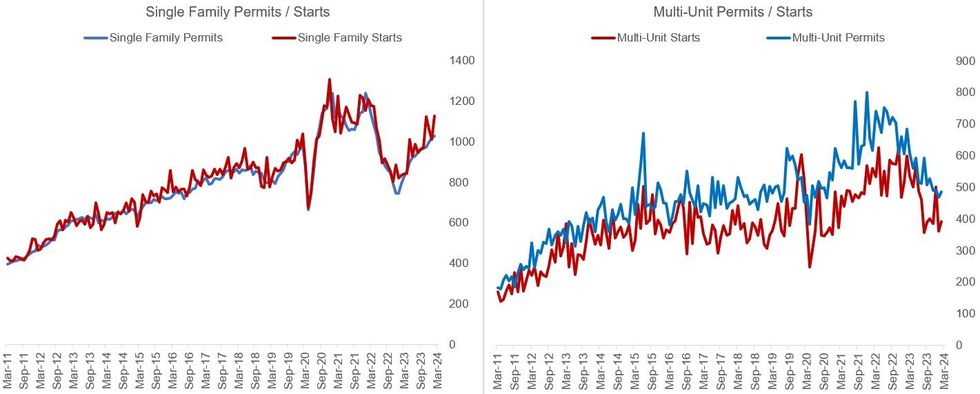

February housing starts and building permits came in stronger than expected, with January's figures also revised upward - but the divergence between single family and multi-unit housing activity remains stark.

- Total Starts totalled 1,521k on an annualized basis (1,440k expected, 1,374k prior - revised up 43k). Permits came in at 1,518k (1,496k expected, 1,489k prior - revised up 19k). That meant Starts grew 5.9% Y/Y, with Permits +2.4% Y/Y, suggesting overall housing construction activity is picking up more broadly.

- Looking at the underlying data though, single family permits made up 1,031k of permits highest since May 2022 and the 13th consecutive monthly increase, with multi-units just 487k - a slight uptick from January but in a broader downtrend that started in mid-2022.

- Likewise, single-family starts came in at 1,129k - the highest since April 2022 - while multi-unit starts remained below the 400k mark for another month (392k), and well below late 2022/early 2023 levels.

- The divergence in the series continues to be explained by rising interest rates offsetting investor interest in multi-unit housing, while single-family activity is gaining as homeowners are unwilling to move and refinance lest they give up their low-rate fixed mortgages, pushing new home demand higher.

- While there is a disinflationary impact from multi-family supply coming online - 5+unit completions hit the highest since 1974 in February - resilience in real housing market activity in the face of tighter monetary policy will remain a confounding factor in the FOMC's thinking on the potential for rate cuts later this year.

Source: Census Bureau, MNI

Source: Census Bureau, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok