Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

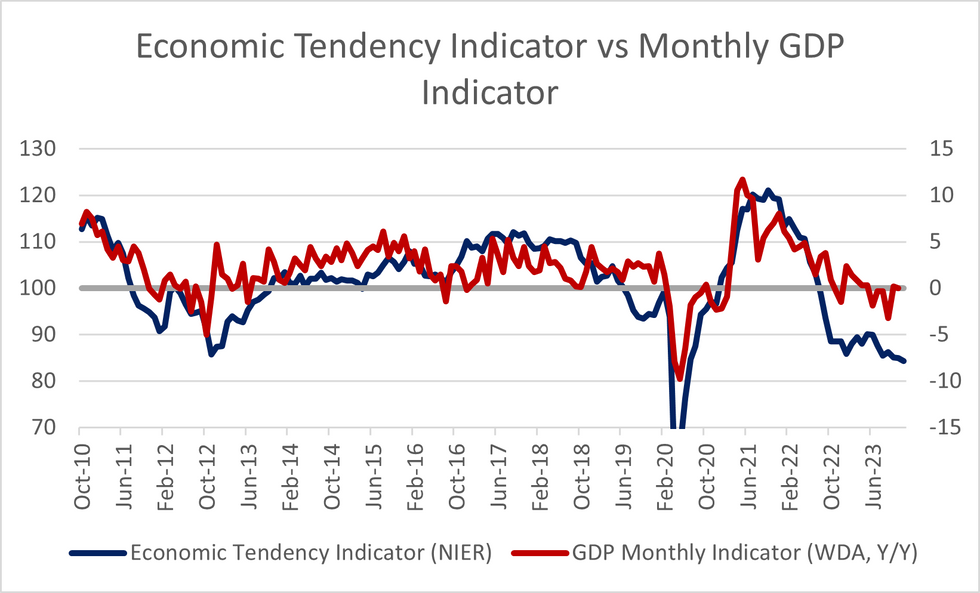

The December Economic Tendency Indicator did not provide meaningful enough signals to change the Riksbank's current course of action.

- While there was stickiness in pricing plans across sectors (other than in construction), yesterday's speech from Riksbank Governor Thedéen suggested that the hiking cycle is likely at an end.

- Confidence remains weak overall. The headline indicator printed at 84.3, from an upwardly revised 84.9 prior. Consumer confidence remained at a low level at 74.5, but rose for the third consecutive month to 74.5 from an upwardly revised 73.2 prior. Both measures remain below the 90 threshold indicating "much weaker growth than usual". • The press release notes that construction sector "production plans have not been as pessimistic since 1996", while manufacturing confidence also fell (to 95.1 vs 99.1 prior). Retail trade and services both saw upticks in confidence to 92.1 (vs 88.3 prior) and 85.3 (vs 83.0 prior) respectively.

- The confidence indicators were corroborated by employment expectations, with retail/services expectations rising and construction/manufacturing expectations falling.

- Consumer 1Y ahead inflation expectations saw a meaningful step down to 6.5% Y/Y (vs 7.1% prior) - ending 4 months above 7% Y/Y.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok