Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

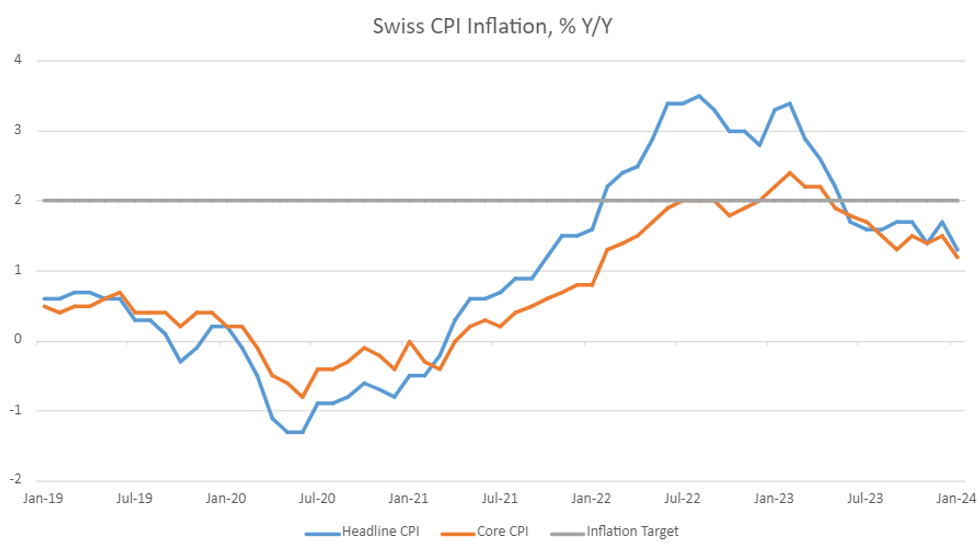

Swiss December CPI came in clearly softer than expected at +1.3% Y/Y (vs +1.7% cons and prior) and +0.2% M/M (vs +0.6% cons; 0.0% prior). The core reading came in at +1.2% Y/Y (vs +1.6% cons; +1.5% prior).

- Looking at individual components, both goods and services prices inflated on a monthly basis, coming in at +0.1% M/M (-0.5% prior) and +0.2% M/M (+0.4% prior), respectively.

- On a more granular level, inflation was driven higher by electricity (+17.8% M/M, contributing 0.33pp to the headline M/M figure), hotels (+10.6% M/M, +0.17pp), and car insurance (+4.7% M/M, +0.03pp). Negative impacts came from air transport (-8.6% M/M, -0.07pp), woman's coats and jackets (-15.8% M/M, -0.04pp) and supplementary accomodation (-4.5% M/M, -0.03pp).

- The SNB expected Swiss inflation to tick up after its last press conference in December on higher electricity prices, rents, and VAT (which increased to 8.1% in January from 7.7%). Even though the "housing and energy" category contributed to headline inflation positively on a monthly basis, partly due to the expected electricity price uptick materializing at least to some extent, it disinflated further on a yearly basis, however, coming in at +2.5% Y/Y (+3.3% Y/Y prior). Additionally, some of the categories driving the upside surprise in December, in particular air transport, contributed negatively in January.

- On a larger picture, there are now clear downside risks to the current SNB inflation forecast for Q1, which stands at 1.8% Y/Y (2.0% for Q2 2024), mirroring SNB's Jordan's recent comments on inflation being negatively impacted by the stronger CHF.

- The CPI basket was reweighted for 2021-2023 expenditure, removing some of the early Covid expenditure shifts of 2020, but still includes periods with greater goods versus services consumption than indices that are reweighted purely based on one year's expenditure.

MNI, FSO

MNI, FSO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok