Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

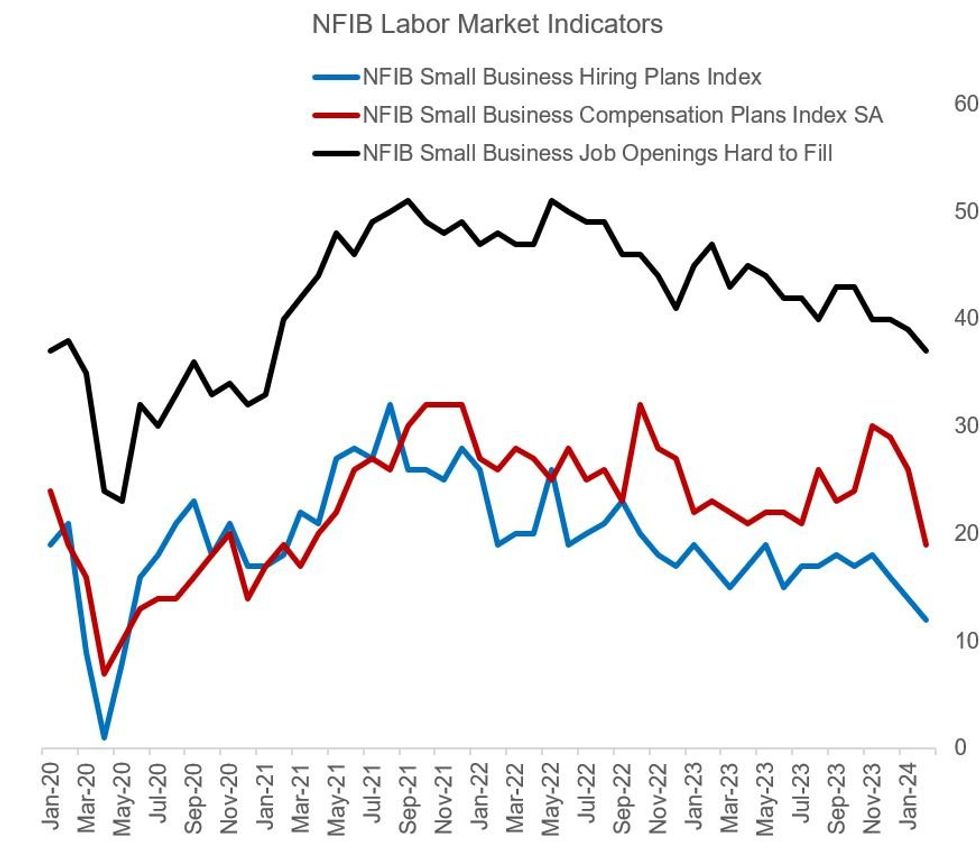

The headline Optimism index in February's NFIB Small Business Economic Trends survey unexpectedly dipped to 89.4 from 89.9 in January, defying consensus expectations for a tick up to 90.5 and the weakest reading since May 2023. Overall the internals of the report were soft, particularly regarding forward-looking expectations for hiring and wages - another set of evidence that the US labor market is loosening from very tight conditions in 2021/22.

- The net percentage of small businesses planning to hire in the next 3 months fell to 12%, down 2pp to the lowest since May 2020. 37% of firms reported that they had job openings they couldn't fill, 2pp down from January and the lowest since January 2021.

- Against this backdrop, wage pressures appear to be diminishing: the net percentage reporting raising compensation fell 4pp to 35%, the lowest reading since May 2021, while just 19% on a net basis plan compensation increases - down 7pp and the lowest since March 2021.

- This brought the percentage of firms reporting labor quality as their "biggest problem" down 5pp to 16% - the lowest since April 2020. Those citing labor costs as their "biggest problem", conversely, ticked higher to 11%, 2pp below the Dec 2021 high of 13% - and 23% cited "inflation", up 3pp and replacing "labor quality" as the "biggest problem".

- While the latter gives some inflationary undertones to the report, it should be noted that the net percent raising selling prices fell 1pp to 21%, lowest since January 2021.

- Given that much of the weak labor data data was released separately last week in the monthly NFIB jobs report, today's release brought fairly limited market reaction, but should add to the case for Fed rate cuts later this year.

Source: NFIB, BBG, MNI

Source: NFIB, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok