Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GILTS

Gilts rally after core global peers regained some poise overnight. The rally fails to test 97.00 in futures, leaving the contract at 96.82 last.

- Yesterday’s sell off deepens the bearish technical threat. Bulls need to retake yesterday’s high (97.43), Meanwhile, a break of yesterday’s low would expose support at 96.25, a Fibonacci retracement.

- Yields are 1.0-2.5bp lower across the curve, bull flattening.

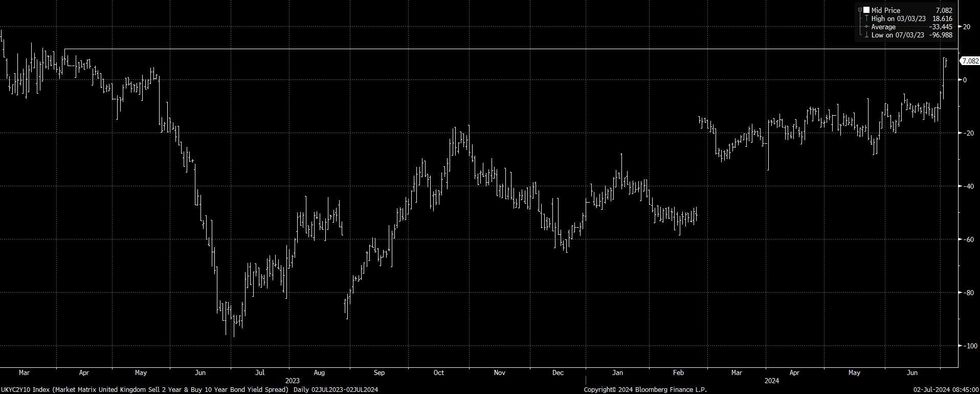

- This comes after yesterday’s steepening saw 2s10s close above 0bp for the first time since May ’23. The April 5 ’23 high (11.4bp) is the next target on that curve.

- 5s30s hit a fresh multi-month high on Monday but failed to challenge YtD highs.

- BRC shop price index data showed the shallowest Y/Y rise since late ’21, +0.2%.

- Still, the report noted that “the latest results reveal a slowdown in consumer optimism compared to recent months.” The post-election trajectory in confidence will be worth watching.

- GBP4bn of Mar-27 gilt supply is due from the DMO this morning.

Fig. 1: UK 2-/10-Year Yield Curve (bp)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok