Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

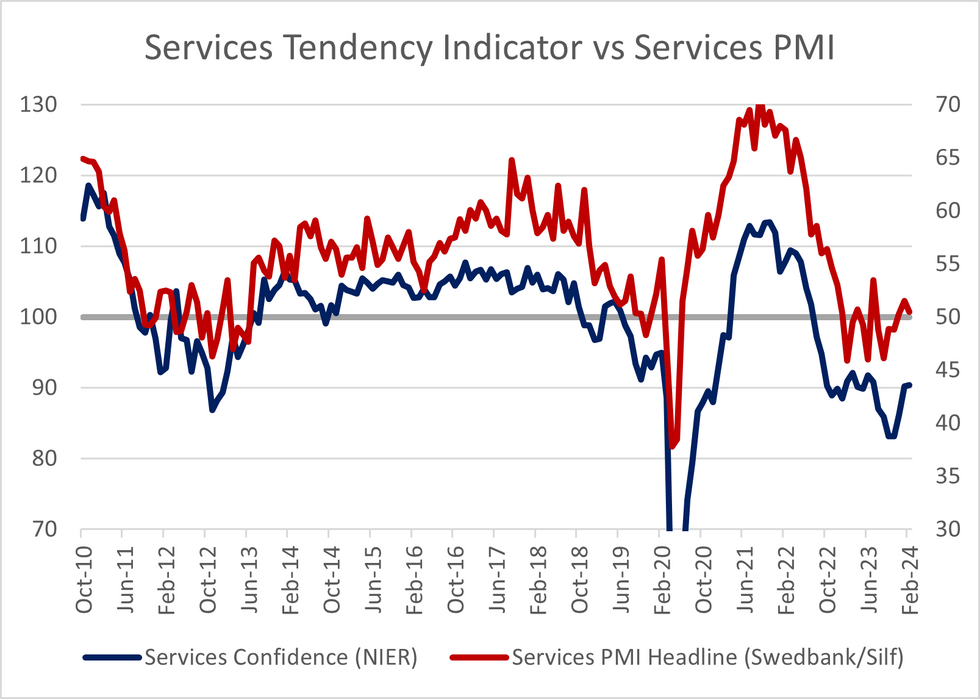

The Swedish February services PMI fell to 50.5 (vs a downwardly revised 51.5 prior). Details suggest a stagflationary report, but the inflation signals are in contrast to recent survey and inflation data.

- The survey continues to indicate a relatively more optimistic picture that the Economic Tendency Indicator (ETI), though we note that this has been the case for much of the last decade.

- Supplier input prices rose to 62.4 (vs 56.4 prior, the highest since August 2023). This comes in contrast to the recent deceleration in January services CPI (to 4.9% vs 6.4% prior) and the services business pricing plans indicator in the February ETI (to 13 from 23, versus a historical average of 11).

- Employment fell to the lowest level since October 2020 (to 46.1 vs 50.3 prior), consistent with the recent drift upwards in the unemployment rate.

- One bright spot in the survey is future business volume, which rose to 62.0 (vs 55.5 prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok