Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

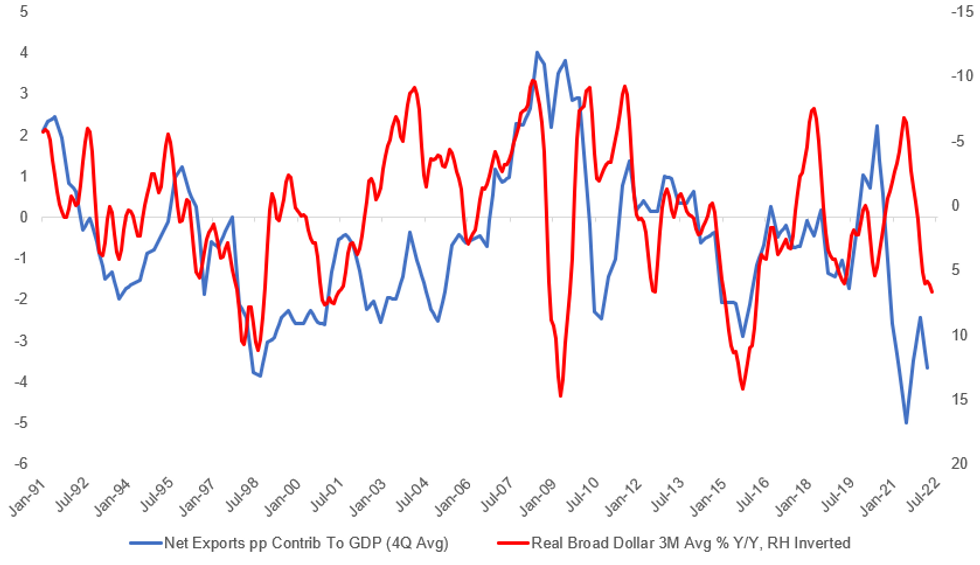

The chart below shows the 4-quarter rolling average of Net Exports' contribution to US GDP, vs the change in the real broad dollar index (inverted, in red).

- The large negative contribution in the last 2 years is basically one-off pandemic-related as goods imports soared during lockdown amid extremely strong domestic demand (and subdued foreign demand). In this case, unusually, the weaker dollar came hand-in-hand with a bigger drag from exports.

- While the historically large drags from net exports won't persist, likewise, we would expect continued USD strength to maintain pressure on the external sector.

- The broad real index is up about 7% Y/Y to May, implying a modest but growing drag ahead. NY Fed's trade model, for one, implies that for a 10% dollar appreciation shock at the beginning of year 1, net exports drag down GDP by 0.5pp in year 1 and 0.7pp in year 2 (versus baseline, and assuming the appreciation persists).

- Consensus sees real export growth easily exceeding import growth over the next several quarters - any disappointment on that front could weigh on net exports and overall GDP expectations.

Source: BEA, Fed, MNI Calculations

Source: BEA, Fed, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok