Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

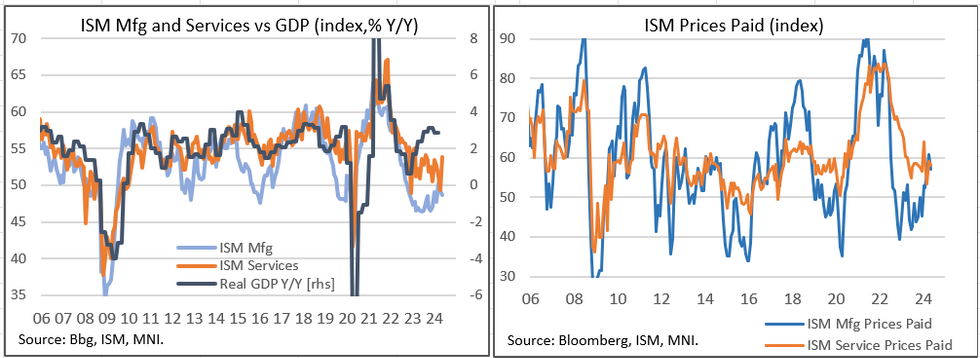

The ISM Services report for May was surprisingly strong, with the headline index rising 4.4 points to 53.8 - the biggest one-month rise since January 2023, the highest reading since August 2023, and suggesting that April's sub-50 reading was an anomaly.

- This was a "goldilocks" report in the sense that activity indices were steady/higher even as the prices subindex moderated (a still-high 58.1 but down from 59.2 prior). Notably, the business activity/production category soared 10.3 points to 61.2 - joint-highest since December 2021.

- New orders rebounded 1.9 points to 54.1, new export orders soared 13.9 points to 61.8 (an 8-month high, and the biggest one-month increase since April 2023) with imports dropping 10.8 points to 42.8.

- The employment category, which will be very closely looked at ahead of Friday's nonfarm payrolls report, rose 1.2 points to 47.1, partially reversing a 2.6 point drop in April but still contractionary and below the Q1 average of 49.0.

- Backlogs and inventories grew slightly more slowly.

- The contributor anecdotes weren't exactly exuberant, with several citing softer demand and higher interest rates clouding the outlook.

- But along with a strong S&P PMI Services reading (+3.5 points to 54.8, confirmed in the final), May looks like it saw a solid rebound in services sector activity - in contrast to manufacturing, which saw a softer ISM reading.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok