Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Sweden Macro Signal - May 2024: Recovery In Sight

MNI Point of View: Recovery In Sight

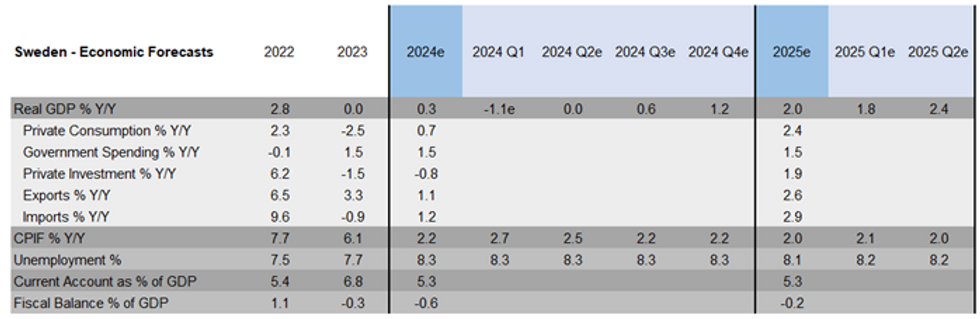

The Riksbank became the second G10 central bank to ease policy rates at its May meeting, cutting by 25bps to 3.75%. This decision reflected downside surprises to inflation and a weakening of the labour market, through the weak krona, geopolitics and Fed policy were once again highlighted as risks to the outlook. Economic activity remained subdued in Q1, but “green shoots” (in the Riksbank’s words) are beginning to emerge, supported by improving sentiment and positive real wage growth.

- Economic Activity: Flash Q1 GDP printed unexpectedly weak at -0.1% Q/Q, signalling economic activity remains subdued. However, improving consumer and business sentiment, combined with rising real wages should help support activity going forward.

- Inflation: Has tracked below the Riksbank’s March MPR projections in the last 2 months, and the lower-than-expected March reading was the key factor in giving the Riksbank confidence to cut rates in May. Normalising business pricing plans suggest further disinflation is likely, though the weak SEK remains a concern.

- Labour Market: The Swedish labour market has shown signs of loosening, with increases in unemployment and redundancy notices seen alongside moderations in employment and vacancies. However, these trends are expected to reverse alongside the wider economic recovery in the coming years.

- Monetary Policy: The Riksbank Executive Board unanimously voted to cut the policy rate by 25bps to 3.75%, with the domestic macroeconomic data since the March meeting having met the required threshold to begin easing.

- Medium-Term Outlook: Expectations for short-term Swedish economic activity have slightly improved for 2024, with a more pronounced recovery expected through 2025/2026. Growth is expected to average 2.0% Y/Y in 2025 and 2.2% in 2026 - slightly below the Riksbank’s forecast - as the restrictiveness of Riksbank policy is dialled back. Annual CPIF inflation is expected to fall below the Riksbank’s 2% target by 2025, while the unemployment rate is expected to remain around 8.3% through 2024, before falling through 2025 and 2026.

Full PDF Analysis:

2024_05_Sweden_Macro_Signal.pdf

Note: 2024 Q1 real GDP populated using the GDP indicator. Figures represent Medians. Source: MNI Consensus based on forecasts entered on Bloomberg, as of May 20, 2024.

Note: 2024 Q1 real GDP populated using the GDP indicator. Figures represent Medians. Source: MNI Consensus based on forecasts entered on Bloomberg, as of May 20, 2024.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.