CONSUMER STAPLES

- Firstly, docs have left unch the wording around Event of default including material subsidiary definition of profits before tax or net assets >10%. This builds our confidence on the initial take (linked below) that Tesco bank sale does not meet thresholds.

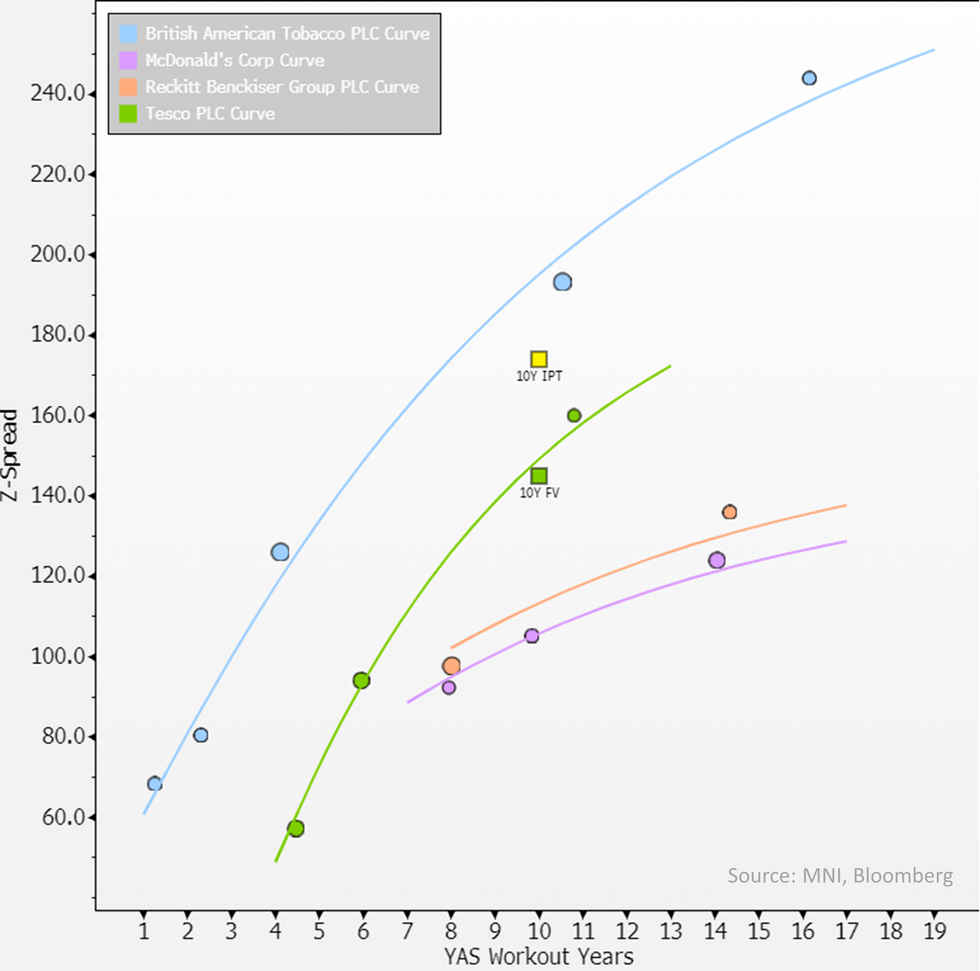

- For those wondering why this is relevant, colour we have is investors pricing in a par call may have contributed to some dislocated moves (see €29/31s spread - the 29s low cash px, 31s high). We do not consider a par call at all likely for now.

- FV is Z+145 & is dragged up by the 0.8y longer 35s trading at Z+160. Both FV and 35s look well wide with former being spread +40 above McDoanld's (Baa1/BBB+). In € 29s are flat to MCD, 31s spread +25 - again we think above par-call plays skewing these spreads and FV spread to MCD somewhere in high single digits.

- Cross check for Tesco wideness is 5s10s curve spread (30/35s) pricing steeper than a Tobacco name, BAT.

210 words