Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BTP

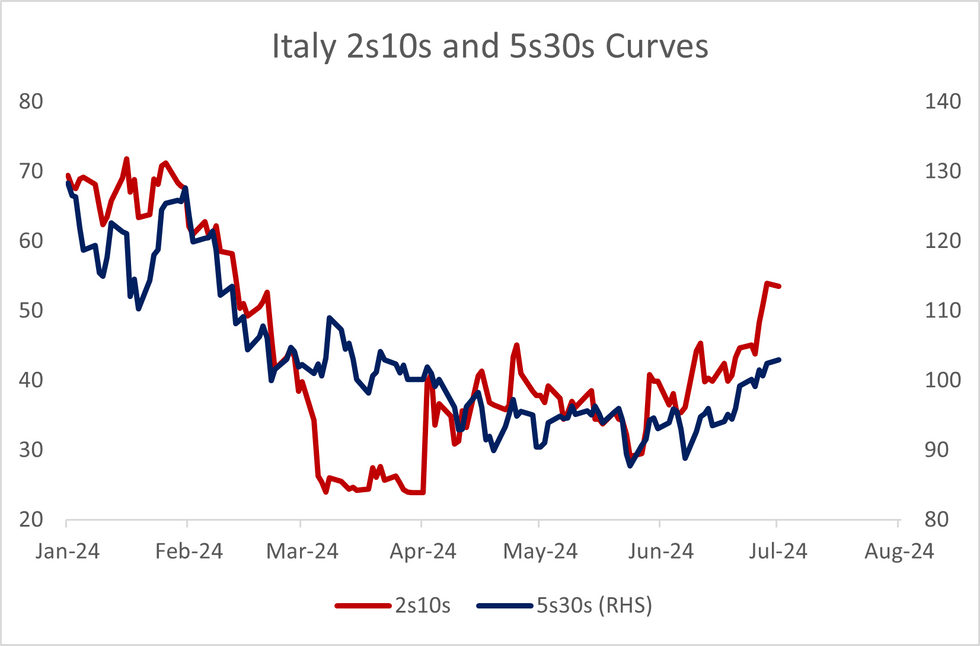

The unwind of some political risk premium tied to the French elections at the medium/long-end has helped contain additional steepening in the 2s10s and 5s30s BTP curves, though both remain close to their steepest level in months. Nonetheless, unfavourable developments in tomorrow’s Q1 domestic fiscal data may provide a catalyst for further steepening.

- Spillovers from the French snap legislative election announcement on June 9th drove curve steepening across Europe through June, with fresh concerns surrounding France’s fiscal trajectory and European Commission policy ramifications taking focus.

- A recent bill granting greater fiscal autonomy to regional governments has also been a point of discussion, with critics concerned with the impact it would have on already-fragile public finances (see here).

- The Italian general budget deficit was 7.4% in 2023, and consensus is for an improvement to between 4.3% (Italian Treasury) and 4.7% (Bloomberg median) in 2024.

- This deficit moderation is expected because of the phase-out of energy support measures and the lower cost of tax credits from the controversial “Superbonus” scheme.

- However, markets may yet demand a heightened yield premium from medium/long-end BTPs, should the Q1 deficit show a lack of improvement from current levels.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok