Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

January trade figures were disappointing, with export growth coming in at -16.6% y/y (-11.1% forecast, -9.6% prior), while imports printed as expected -2.6% y/y (prior -2.5%). The trade deficit ballooned out to -$12.69bn, versus -$9.27bn expected and -$4.69bn prior.

- Export growth continues to trend lower, now at levels last seen in early 2020 (we troughed around -26% in April 2020).

- There is some hope of improved conditions going forward, the first chart below overlays export growth against export expectations from South Korean manufacturers (sourced from the BoK).

- The most recent survey showed a slight uptick after a sharp downturn through the latter stages of 2023. We remain at depressed levels though and while China's exit from CZS should aid demand, the recovery is not expected to be V shaped.

- The consensus looks for real export growth to be back at 3.0% y/y by end of this year (we were at -4.4% in Q4 of last year).

Fig 1: South Korean Exports Versus Manufacturers' Expectations

Source: MNI - Market News/Bloomberg/BoK

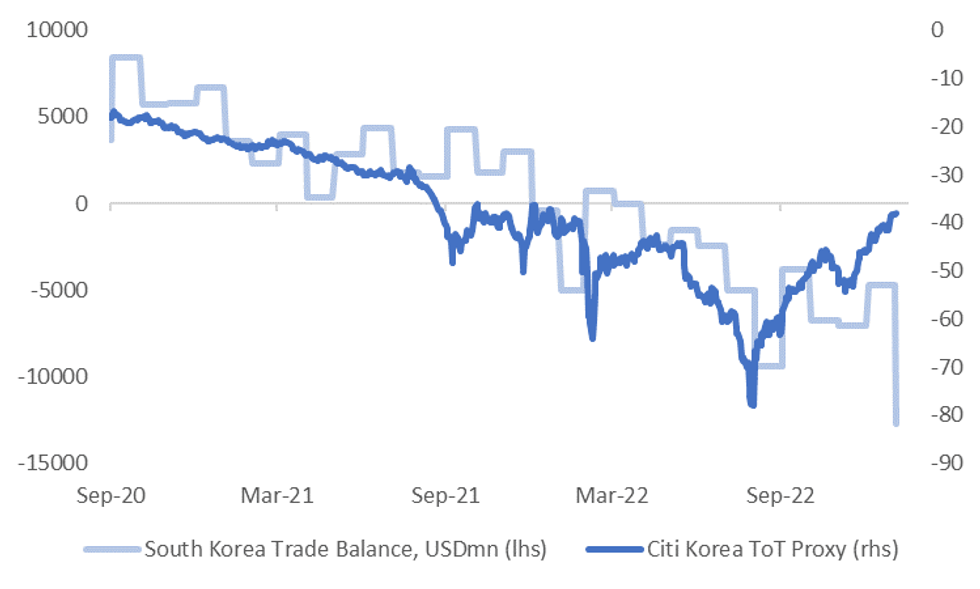

- The relationship between the trade deficit and the Citi South Korean terms of trade (ToT) proxy has weakened, see the second chart below. The trade deficit hit a fresh record wide near -$12.7bn in January. The authorities cited weakness in chip prices and still elevated energy costs as drivers of this result.

Fig 2: South Korea Trade Deficit Hits Fresh Wides Despite Citi ToT Proxy Improving

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok