Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUSSIE BONDS

Early Sydney trade was two-way, with the early richening inspired by an overnight bid in core global FI markets and NZ CPI data that was a little softer than the RBNZ expected.

- Firmer than expected (vs. newswire surveys) domestic CPI data then applied notable pressure, leaving YM -9.0 & XM -4.0 at the close, a touch above their respective session lows. The major cash ACGBs finished 2-10bp cheaper as the wider curve bear flattened. ACGB widened vs. global peers post-CPI.

- The headline CPI metric was a touch below the RBA’s forecast +8% Y/Y, although the trimmed mean metric topped the Bank’s +6.5% Y/Y forecast. Inflation continues to run at particularly elevated levels for this stage in the RBA hiking cycle.

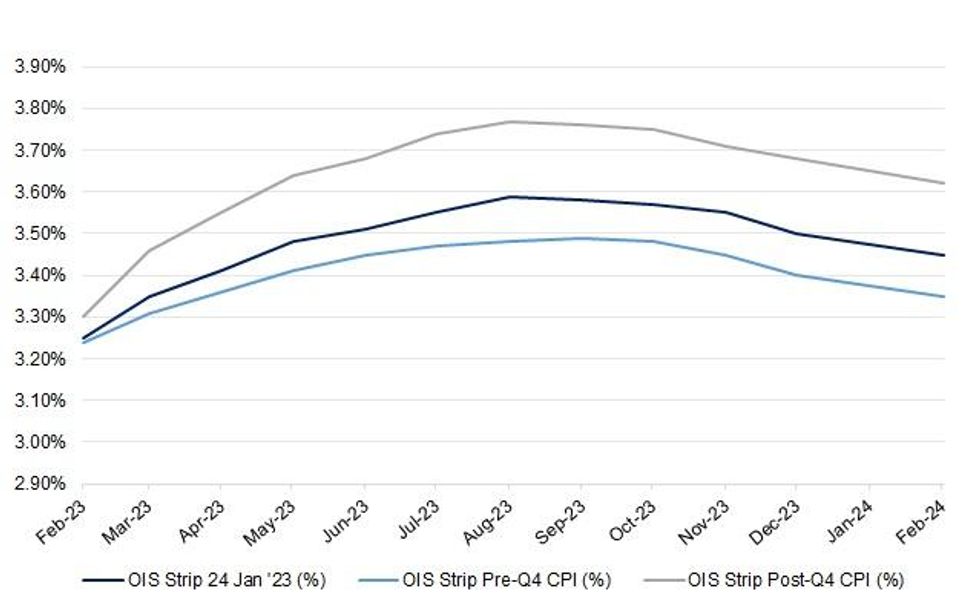

- Bills finished 13-19bp cheaper through the reds, in what was a volatile day for Aussie STIRs. RBA dated OIS now shows ~23bp of tightening for next month’s meeting, almost fully pricing a 25bp hike post-CPI. Meanwhile, terminal cash rate pricing is showing just above 3.75% late in the day after printing below 3.50% in the wake of the NZ CPI release (see chart below for a visual on intraday swings). There hasn’t been any meaningful RBA call changes from the sell-side post CPI.

- Australian markets are closed on Thursday as the country observes the Australia Day holiday.

Fig. 1: Intraday Moves In RBA Dated OIS

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok