Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

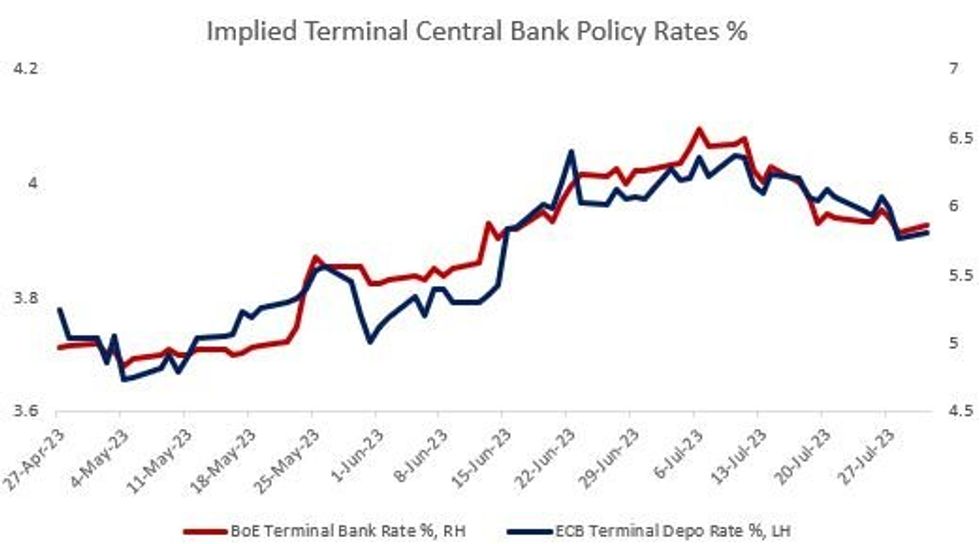

BoE and ECB peak hike pricing ticked higher Monday, partially reversing Friday's drop.

- BoE terminal Bank Rate pricing +6.2bp to 5.86% (86bp of further hikes left in the cycle to Feb 2024). Little related newsflow today (MNI's Policy Team eyes an announcement on QT policy in September), but peak pricing reversed half of Friday's drop. There's just 33bp priced for Thursday's decision, equating to a roughly 1-in-3 probability of a 50bp vs a 25bp raise. 60bp is cumulatively priced through the next two meetings.

- ECB terminal depo Rate pricing +1.2bp to 3.91% (17bp of further hikes left in the cycle to Dec 2023). Slightly stronger than expected Eurozone core Y/Y July flash HICP (5.5% Y/Y, unch from June, and vs 5.4% survey) didn't move the needle, with the narrative seeming to be that multiple statistical distortions leave the case for a further hike ambiguous on purely inflation grounds. Indeed there's just 15bp in cumulative hikes priced through the next two meetings, including 9bp in September.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok