Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

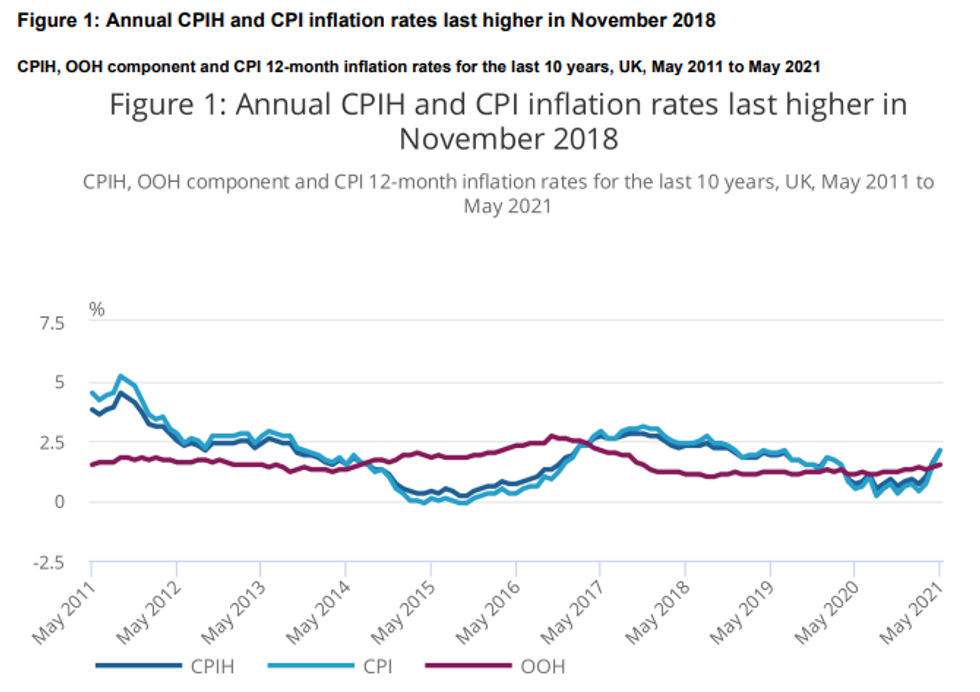

MAY CPI +0.6% M/M, +2.1% Y/Y VS +1.5% Y/Y APR

MAY CORE CPI +0.8% M/M, +2.0% Y/Y VS +1.3% Y/Y APR

MAY OUTPUT PPI +0.5% M/M; +4.6% Y/Y VS +4.0% Y/Y APR

MAY INPUT PPI +1.1% M/M; +10.7% Y/Y VS +10.0% Y/Y APR

- The Y/Y CPI jumped to 2.1% in May, beating expectations (BBG: 1.8%). This marks the second successive increase and the first reading above the BOE's 2.0% target after 21 months of readings below it. The CPI also recorded 2.1% in Jul 2019 and was last time higher in Nov 2018.

- Core inflation rose to 2.1%, its highest level since Aug 2018 and it came in stronger than projected (BBG: 1.5%).

- The largest upward contribution came from transport, adding 0.2pp to price growth, with prices for fuels and lubricants driving the uptick.

- Fuel prices rose significantly in May, mainly on the back of base effects as prices dropped sharply at the same time last year. Annual prices for motor fuels rose 17.9% in May, the highest increase since Feb 2017.

- The second largest positive contribution stemmed from recreation and culture, adding 0.19pp to CPI growth, followed by clothing and footwear which contributed 0.16pp to price growth. The ONS noted that the amount of discounting for clothing fell in May, leading to an upward contribution.

- The largest downward pressure came from food and non-alcoholic beverage prices, reflecting a decline in prices in 2021, while prices rose in 2020.

- Output inflation increased 4.6% in May, marking the highest level since 2012 and it was largely driven by transport equipment.

- Input inflation surged by 10.7% in May, showing the highest level since Sep 2011. Metals and non-metallic minerals led the increase of input PPI.

Source: Office for National Statistics

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok