Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

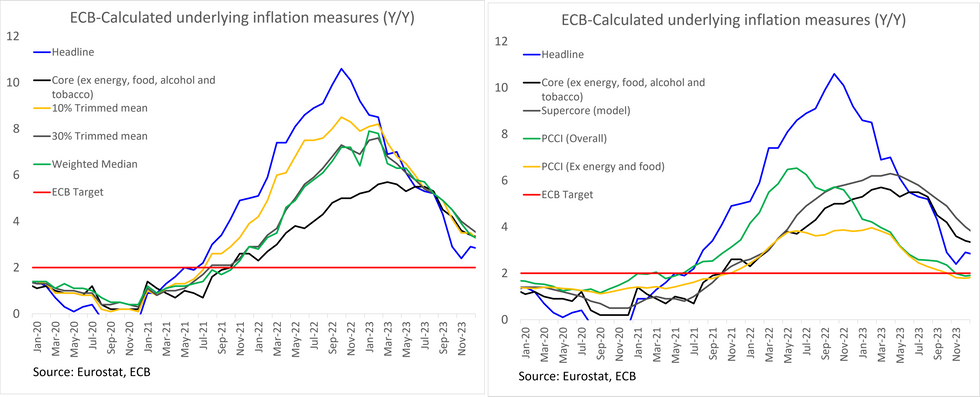

The ECB's underlying inflation metrics for January are likely to be interpreted by policymakers as showing further progress toward the 2% target as they consider when to make the first rate cut.

- While core and headline PCCI (persistent/common component) inflation rose a touch in January, they each remained below 2% for the third consecutive month. Core PCCI was 1.85% Y/Y (vs 1.79% prior) while the headline reading was 1.93% Y/Y (vs 1.88% prior).

- The other underlying metrics (supercore, 10/30% trimmed mean and weighted median) also continued to moderate, with supercore (at 3.7% Y/Y) printing below 4% for the first time since May 2022.

- While certainly still of importance to the ECB, we would note that in a recent speech, ECB Chief Economist Lane caveated the reliability of the signals sent by underlying inflation measures, due to "the relative price shocks that have been triggered by the scale and breadth of the energy shock and the pandemic- and war-related shocks".

- Elsewhere, even though services inflation was sticky at 4% Y/Y in January (for the third month running), MNI's calculations indicate a softening of services momentum. Measured as a 3m/3m saar using ECB data, services momentum moderated to 2.25% (vs 2.54% prior).

- However, the ECB will still want to see moderations in NSA services inflation before progressing with its easing cycle, as it assesses the passthrough of wage pressures into end prices through this quarter.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok