Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

As we've noted previously, even as confidence data (and perhaps activity) may be bottoming out in Q4, the hard data looks to still have some room to fall in the eurozone - especially in the manufacturing / industrial sectors which have so far largely diverged from weaker sentiment.

- To be sure, a technical recession is still the firm expectation: the BBG median forecast for Q/Q GDP shows -0.4% in each of Q4 2022 and Q1 2023, before picking up thereafter.

- But in general the data continue to point to stabilization in expectations - and indeed, the 2023 median BBG real GDP forecast has remained at -0.1% since late October, having plummeted from 2.5% at the outset of the Russia-Ukraine war.

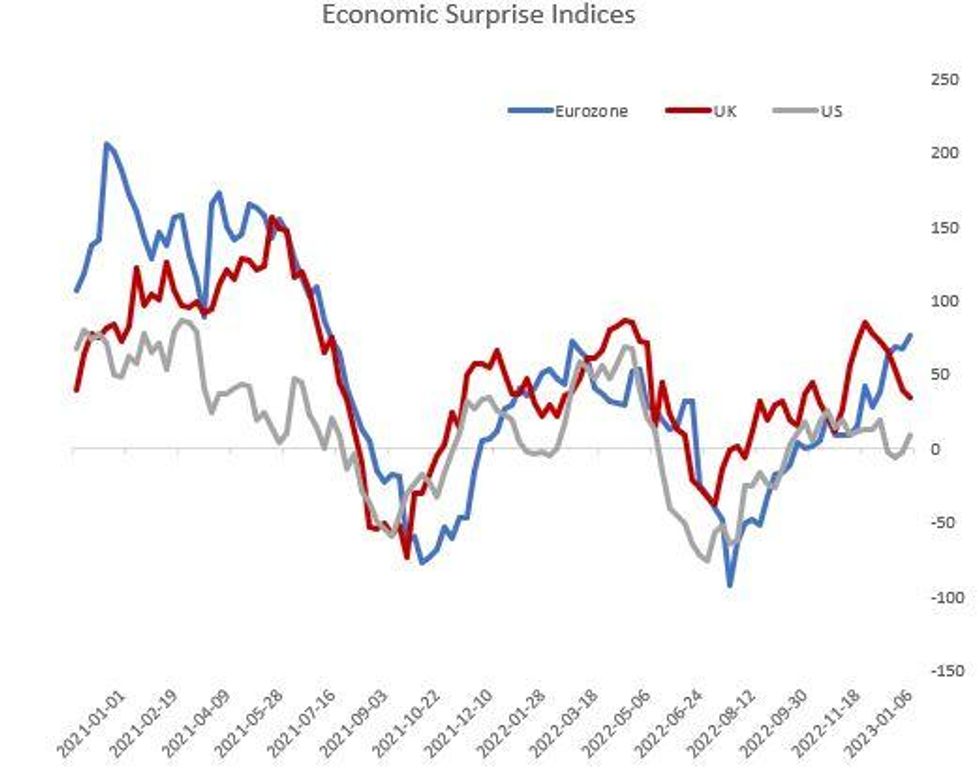

- Eurozone economic readings are currently surprising to the upside to the greatest degree since summer 2021, per Citi's economic surprise indices.

- This marks a recent divergence from the UK (where data had briefly upwardly surprised in Oct/Nov as expectations may have been unduly depressed by the fiscal/Gilt turmoil) and the US (where activity data has been solid but mixed with good labor market data offset by weak manufacturing and housing).

Source: Citi Economic Surprise Indices, MNI

Source: Citi Economic Surprise Indices, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok