Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

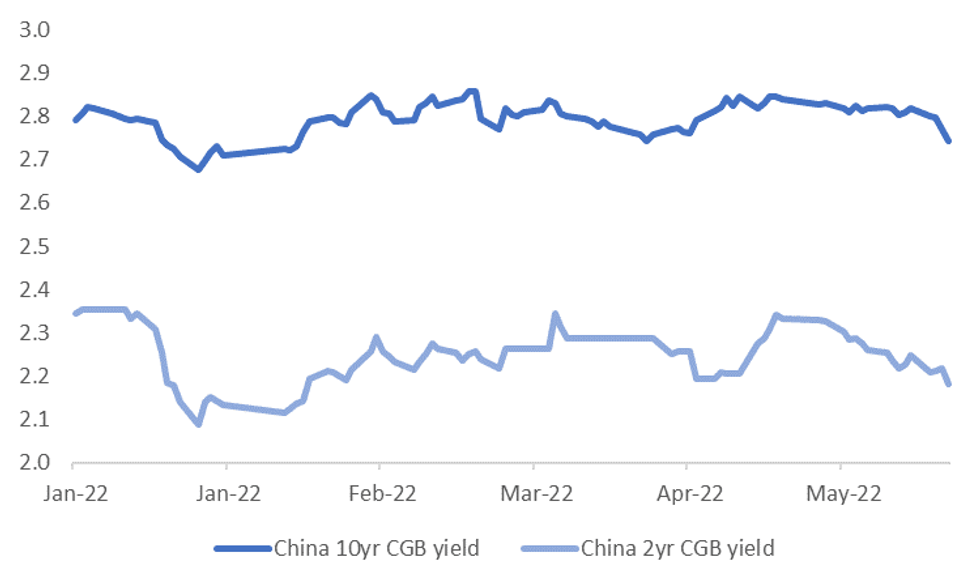

Renewed China growth fears are driving fresh downside in onshore Chinese yields, see the chart below.

- The 2yr and 10yr saw decent moves lower yesterday, with both tenors not too far away from multi-month lows. These moves came after Premier Li's warning around 2022 growth challenges on Wednesday.

- Further downside pressure in yields is likely to remain in focus today.

Fig 1: China 2yr & 10yr CGB Yields Seeing Fresh Downside

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

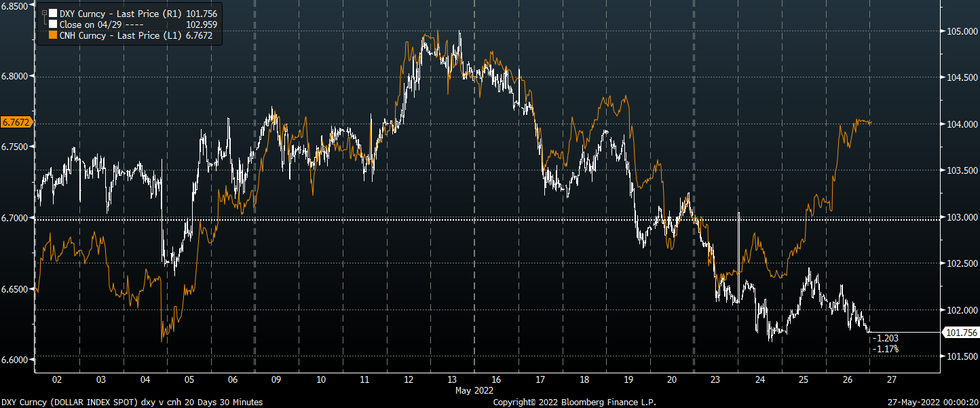

- Such a backdrop is starting to drive a wedge between USD/CNH and the DXY index, see the second chart below.

- We have seen meaningful underperformance of CNH this past week when compared to some of the major currencies. CNH has fallen slightly more than 1% against the USD, while JPY has gained 0.65% and EUR +1.60% (vs. the USD) over this period.

- Further CNY weakness in trade weighted terms is likely to remain a theme until the domestic macro picture in China finds a firmer footing.

- The USD/CNY fix will also be eyed today, given stronger depreciation pressures seen in the last 2 sessions. Note that USD/CNY is still well below recent highs of 6.80+.

Fig 2: USD/CNH & DXY Divergence

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok