Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

Headline trade figures for May surprised on the upside, underlying a resilient BoP picture for China, at least on the trade side. This should be supportive of CNH.

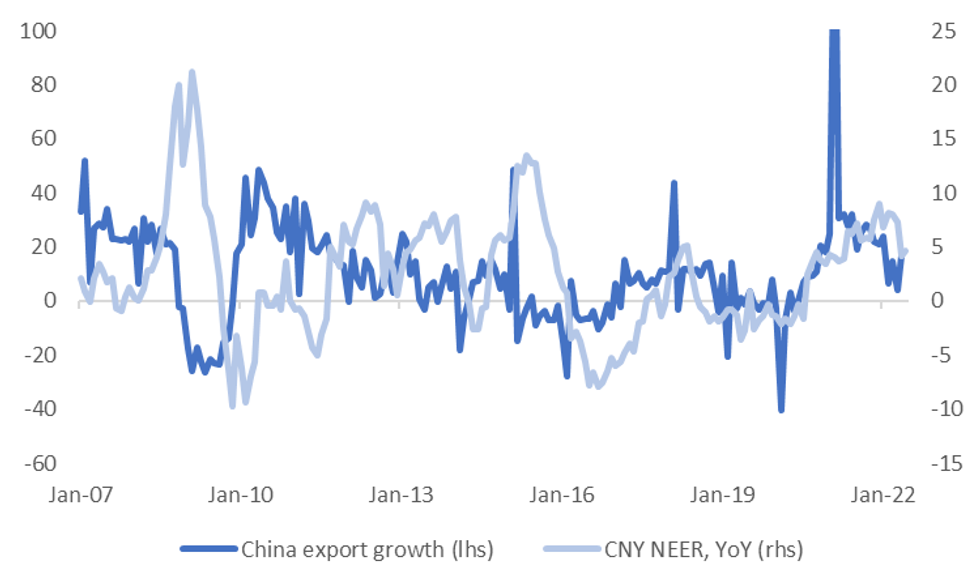

- Export growth printed slightly more double market expectations at 16.9% (8.0% expected). Import growth was less buoyant but still above expectations (4.1% versus 2.8% expected).

- Importantly, the rebound in export growth brings it more into line with CNY NEER YoY momentum, particularly compared to earlier in the year, see the first chart below. The NEER looked too strong in these months, relative to the export trend, but this is less the case now.

Fig 1: China Export Growth & CNY NEER YoY

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

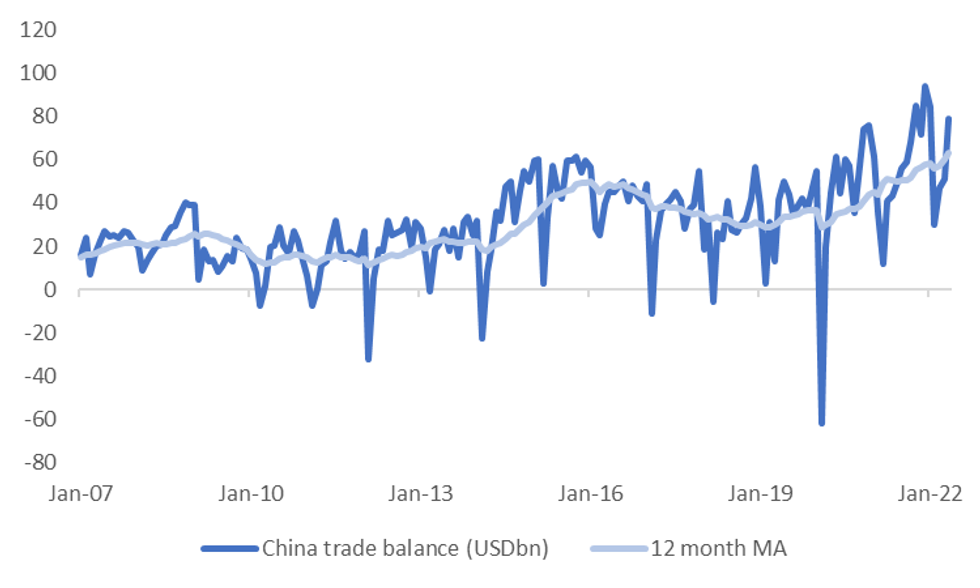

- The trade surplus also surprised on the upside by just over $20bn, coming in at $78.76bn, versus $57.70bn expected. As the second chart below highlights, the 12 month moving average of the trade surplus is still trending higher.

- In many ways China's covid zero strategy boosts the underlying trade surplus position, via dampening import growth. Export growth has comfortably outperformed import growth over the past 3 months.

- Higher trade surpluses should swell corporate China's FX deposit base. This is another factor which can help curb USD/CNY upside pressures.

- USD/CNH is comfortably off its earlier highs, tracking in the low 6.6800, after reaching close to 6.7100 on negative Covid related headlines. Broader USD weakness is helping, with USD/JPY falling back below 134.00.

Fig 2: China Trade Surplus Still Trending Higher

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok