Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FOREX

The USD BBDXY index sits just a touch higher for the session, last near 1254. We are down from earlier highs as the yen received some support after the BoJ reduced its bond buying pace modestly compared with late April.

- USD/JPY looked set to challenge the 156.00 level but the reduced pace of bond buying in the 5-10 tenor aided sentiment. The pair pulled back to 155.52, but didn't see any further follow through. We sit back at 155.75/80, unchanged for the session.

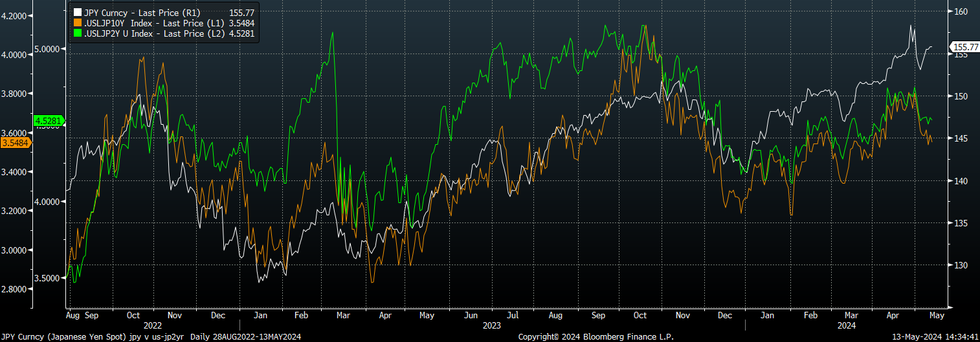

- Japan yields are marching higher, which is weighing on US-JP yield differentials, particularly at the back end of the curve. USD/JPY looks too high relative to such trends, see the chart below, although broader USD sentiment has mostly remained firmer today. Our Tokyo policy team notes the central bank could hasten the policy tightening process given the weak yen backdrop (see this link).

- USD/CNH has climbed above 7.2400 amid weaker data and fresh easing expectations. Higher US tariff prospects have weighed.

- NZD/USD is back close to 0.6000 post a further easing in Q2 inflation expectations. Some support was evident around this figure level though and the onshore rate impact has been limited. AUD/USD is also down, albeit outperforming NZD at the margins. The pair was last under 0.6600. We saw the AUD/NZD cross spike above 1.0990 on the weaker inflation expectations outcome but we have since lost momentum.

- Later the Fed’s Mester and Jefferson discuss central bank communications. In terms of data there is just US NY Fed 1-year inflation expectations for April. The Eurogroup meeting is being held and the ECB’s Buch is scheduled to speak. The focus this week will be on Wednesday’s US April CPI release.

Fig 1: USD/JPY & US-JP Yield Differentials

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok