Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SGD

Singapore Feb exports showed a sharp -8.0% m/m fall (versus -0.5% forecast). Still, y/y momentum was close to expectations at -15.6% (-15.8% forecast and -25.0% prior). Electronic exports remained near recent lows at -26.5% y/y, -26.8% prior (there is no consensus estimate for this print).

- The m/m decrease was driven in part by a plunge in ship related exports, which may reverse somewhat next month. Still underlying trends don't appear to have changed.

- The level of tech related exports continued to trend lower as well.

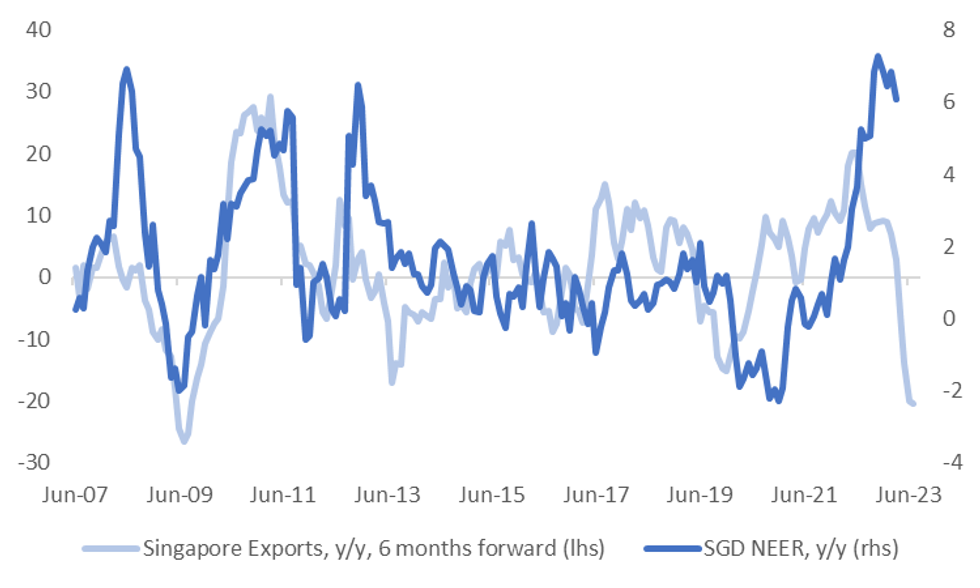

- The chart below takes the 3 month moving average of headline exports in y/y terms. We are still running around -20% y/y, with the SGD NEER (the other line on the chart) looking too elevated still, albeit edging down off recent highs.

- The SGD NEER (per Goldman Sach estimates) slumped as global tightening expectations unwound late last week/early this week, but has been steadily improving since then. We were last near -0.90% from the top end of the band (we were -1.3% at the start of the week).

Fig 1: SGD NEER Y/Y & Export Y/Y Trend

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok