Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

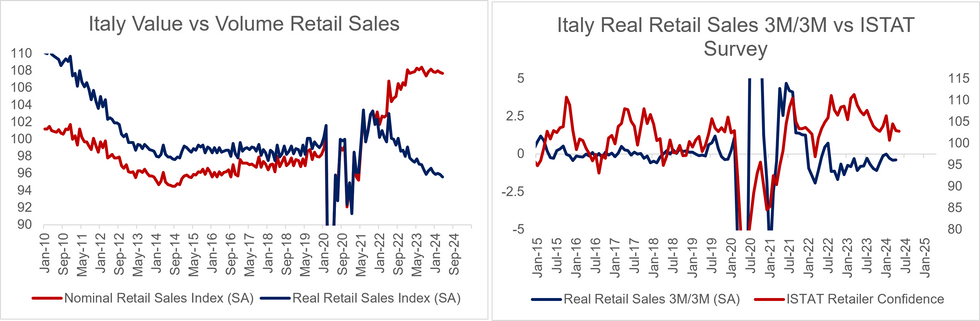

Italian real retail sales fell 0.3% M/M SA (vs -0.1% prior) in April, while nominal sales fell 0.1% M/M SA (vs a two tenths downwardly revised -0.2% prior).

- On a 3m/3m basis, real sales fell 0.4% in April, now the 21st consecutive negative monthly reading for this series.

- The wedge between the nominal and real sales indices grew to 12.1 points (vs 11.9 prior and a 2023 average of 10.9).

- We would expect this wedge to stop widening in the coming months, with core HICP continuing to moderate and the strong labour market helping underpin household consumption.

- ISTAT retail sentiment also remains above the long-run average, although it has fallen in the last two months to 102.8 (vs 104.5 in March).

- Food sales again drove the weakness of the overall index in April, falling 0.7% (vs -0.8% prior). Non-food sales also fell 0.1% as in March.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok