Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUD

AUD/USD spent most of the post Asia close on the back foot. The pair couldn't sustain levels above 0.7150 and we hit lows just under 0.7070 in NY. We aren't too far away from those levels now, last 0.7075/80. This is fairly close to levels that prevailed around the time of Wednesday's Fed meeting. The A$ was the third worst performer in the G10 space, down 0.85% for Thursday's session, with only NOK and GBP falling more.

- The sharp pull back in EU and UK yields (-20/-30bps in the 10yr) post their respective central bank decisions helped the USD rebound, as the markets start to price in/think about pivots in these regions as well.

- This weighed on AUD, with JPY the only G10 currency rising against the USD for Thursday. Equity sentiment was positive (SPX +1.47%) but this didn't aid risk appetite. AUD/JPY is back to the low 91.00 low, near the simple 50-day MA (91.02).

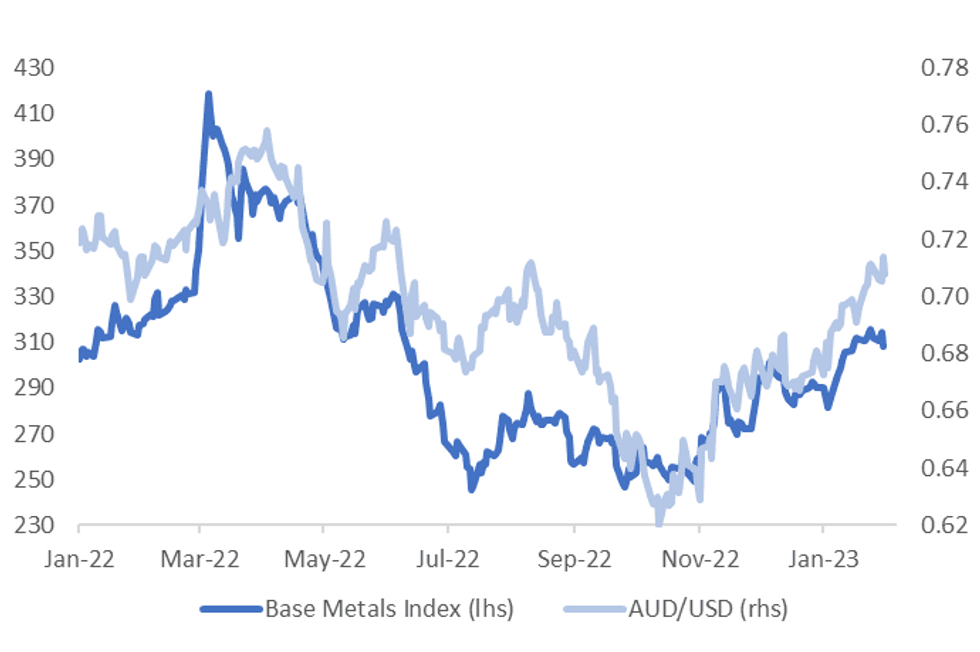

- Commodity indices stayed close to flat in terms of Bloomberg aggregates. These indices failed to rally on Thursday post the Fed. The chart below overlays AUD/USD versus base metal prices, which are now less supportive for the currency. Iron ore is also back to $122/ton.

- On the data front today, the final services PMI reading for Jan is due, along with home loan data (market forecast is -3.0% m/m, -3.7% prior).

Fig 1: AUD/USD Versus Base Metals

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok