Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

RUSSIA

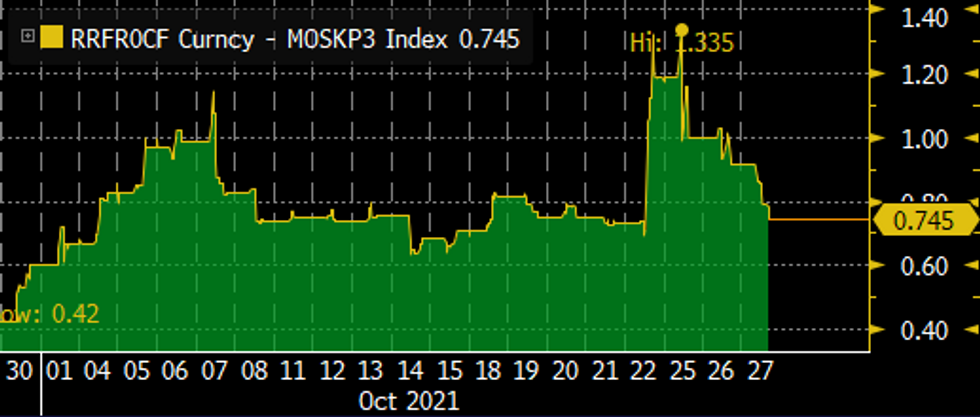

- * After an initial shock following Friday's more hawkish CBR, 3x6 FRA-Mosprime spreads have moderated from a high of +133bp, to a more even +74.5bp. In today's session, the spread has compressed -17bp from +91.5 leading into weekly CPI.

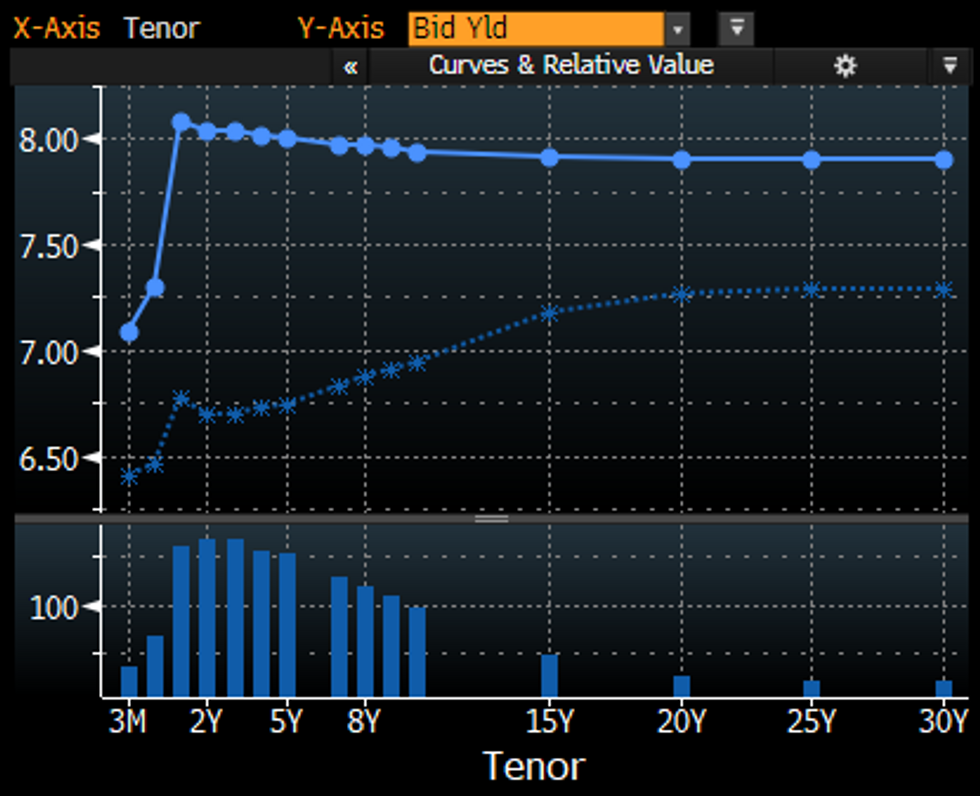

- Since September, weekly inflation has continued to rise unabated, supporting elevated market expectations as headline CPI continued to develop above the CBR's forecast - necessitating an incrementally tighter policy stance (+350bp in hikes thus far). This has also been reflected in front end yields which stand +130bp higher since the start of September with the term structure notably bear flatter.

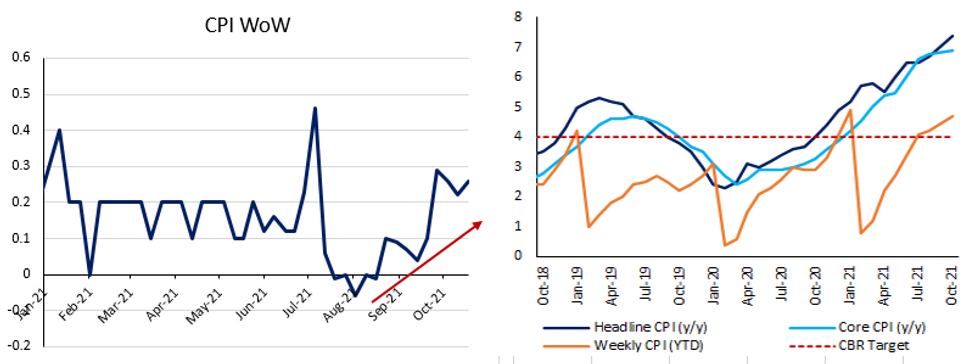

- Last week's numbers registered 0.26% WoW & 5.98% YTD, and will be monitored closely in the lead-up to the next CBR meeting to gauge the magnitude of the bank's next move. At present, forward rates seem to be aligning with the possibility of a +50bp hike in November with the option for +25bp in December or a one and done +75bp hike.

- Given the elevated uncertainty in the inflation outlook and the CBR's diminished credibility in forecasting a peak (which has been fuelling higher expectations), the CBR will not likely wish to be seen as letting up just yet with the signal becoming unequivocally hawkish in the last meeting.

- Hence, the former scenario of a more extended period of hikes seems more palatable at this juncture, but seems a bit conservative and may be more closely aligned with two +50bp hikes for a terminal rate in the 7.75-8.00% range. However, the size of the next move remains highly uncertain and will likely still be contingent on the development of pricing pressures in the coming weeks - making these weekly metrics all the more important.

OFZ Curve Chg form 01 sept

OFZ Curve Chg form 01 sept

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok