Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SGD

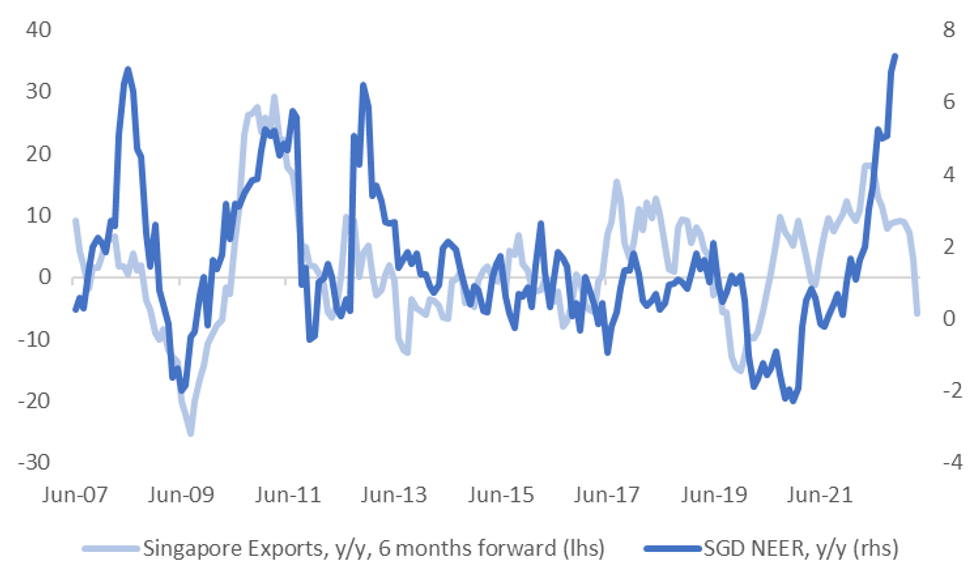

Earlier released November export data surprised on the downside. Exports fell -9.2% m/m (-2.0% forecast), with October revised down a touch, while the y/y printed at -14.6% y/y (-6.5%) forecast. Electronic exports were noticeably weaker at -20.2% y/y, although other major components of exports recorded y/y falls.

- Weakness in Singapore exports brings it into line with trends in other heavily export orientated economies such as South Korea and Taiwan.

- The chart below plots y/y Singapore export growth (smoothed), pushed forward 6 months, against y/y change in SGD NEER. At face value this suggests the best part of NEER gains may be behind us.

Fig 1: SGD NEER Y/Y Versus Singapore Export Growth Y/Y (6 Months Forward)

Source: MAS/MNI - Market News/Bloomberg

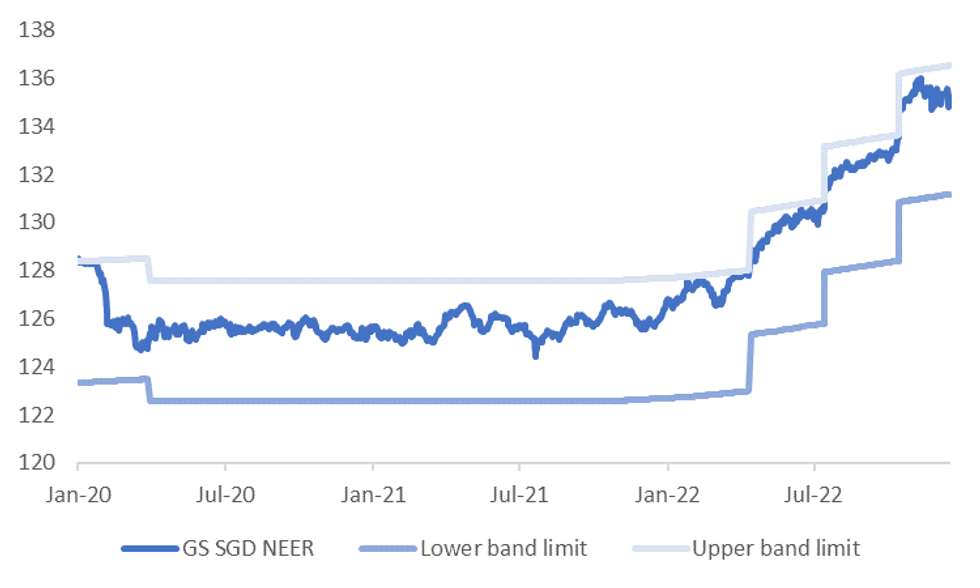

- Of course, future MAS policy decisions will also be heavily influenced by inflation outcomes. Next Friday November CPI prints. The October print came in below expectations, with some signs of a peak in inflation emerging. Note y/y SGD NEER gains, last around +7% is now above the y/y pace for both headline and core inflation.

- If the November print shows further signs that the worst of the inflation uptrend is behind us, the market may speculate the MAS leaves policy settings on hold at the next meeting (which is in April next year).

- Although the market may already be starting to price this. The SGD NEER has been drifting away from the top-end of the policy band, according to Goldman Sachs estimates, following the most recent policy tightening, see the chart below.

Fig 2: Goldman Sachs SGD NEER Estimate

Source: Goldman Sachs/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok