Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

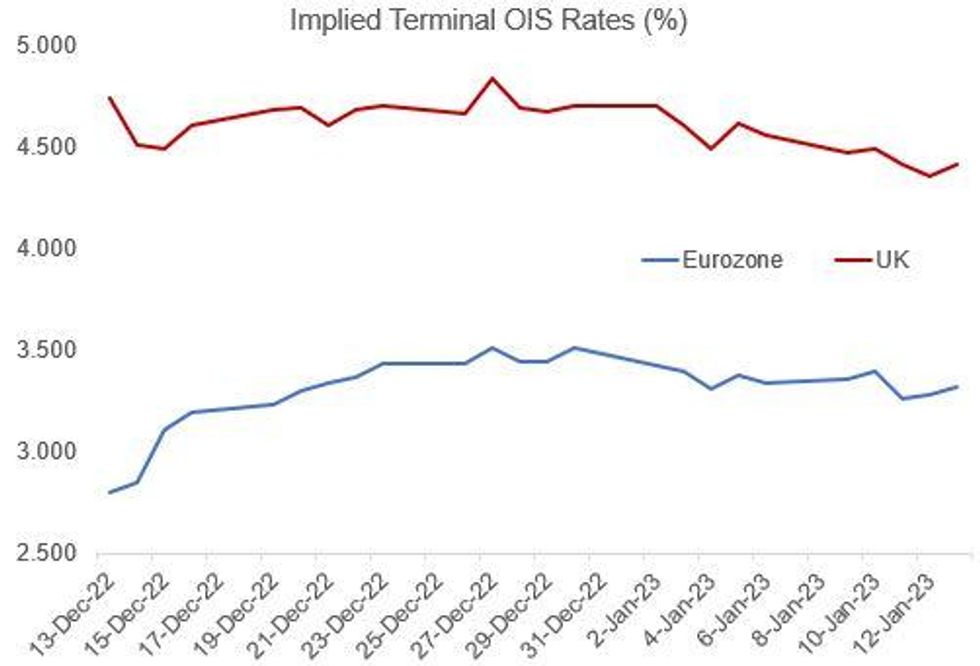

BoE hiking prospects are dimming: while 45bp of hikes is still envisaged for the February MPC, and 76bp for the Feb and Mar meetings combined, the terminal rate is seen being reached after just 97bp of further increases to September.

- The 4.43% terminal Bank Rate implied on Thursday was the lowest since mid-November and down from 4.62% at the end of last week - this week's close is set to be at 4.47%.

Just under 143bp of further ECB hikes are priced in; that is little changed on the week despite the below-expected US CPI figures and the broader fixed income rally. Though there was some volatility: the low was 137bp (early Friday) with a high of 151bp (Tuesday).

- The biggest single mover was MNI's sources piece on Wednesday pointing to Governing Council doves arguing for a slowdown in the hike pace as inflation subsides in the spring - terminal pricing dropped 9bp.

- Meanwhile, Feb ECB hike pricing firmed up slightly this week (95% probability of a 50bp hike vs 25bp), with 91bp of cumulative hikes priced through the March meeting.

Source: BBG, MNI

Source: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok