Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

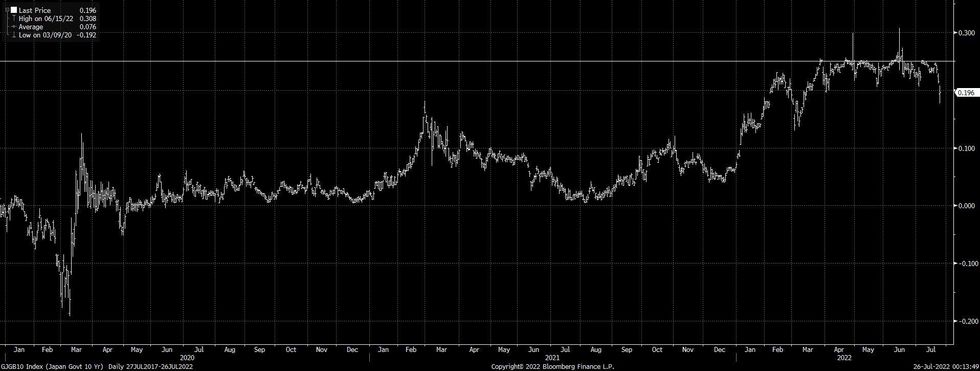

The BoJ has seen off the vigilantes that tested it’s will in mid-June, at least for now, leaving it as the last dove standing in major central bank circles.

10-Year JGB yields touched the lowest level observed since March on Monday, pulling away from the upper end of the Bank’s permitted -/+0.25% trading range.

Fig. 1: 10-Year JGB Yields (%)

Source: MNI – Market News/Bloomberg

Source: MNI – Market News/Bloomberg

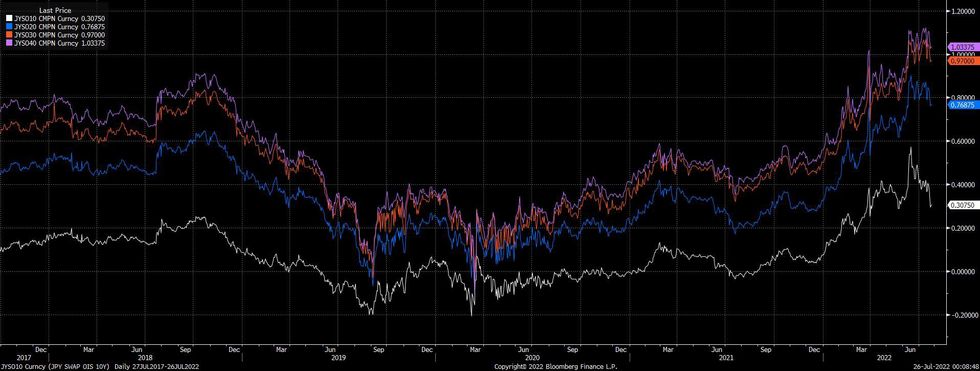

Elsewhere, 10-Year Japanese swap rates have cratered after the BoJ upped its bond buying during June (to a record monthly level), employed some creative tactics when it came to limiting the futures/cash JGB basis blowout and reaffirmed the need to maintain its current policy settings owing to a lack of demand-pull inflation. Wider recession-based worry, centred on the U.S. & Europe, has also helped.

Note that gains in swap rates beyond 10s have been a little stickier given the lack of relative BoJ control further out the JGB curve, although those metrics are still back from cycle highs.

Fig. 2: Japan 10- To 40-Year Swap Rates (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

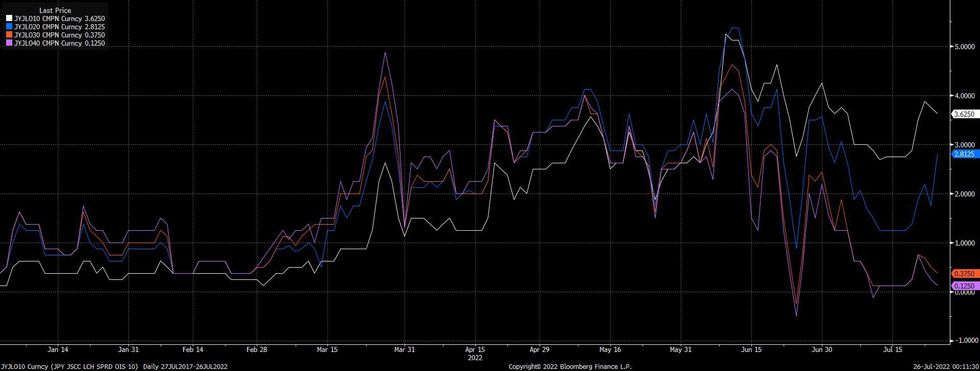

We have documented the recent BoJ-driven covering of short positions in both JGB futures and Japanese bonds on the part of foreign investors in some detail, with that particular investor cohort seen as the main driving force behind the June challenge of the BoJ’s YCC parameters. We would also highlight the post-June BoJ pullback in LCH/JSCC swap spreads covering the 10+-Year zone of the curve, with the moves in these spreads once again indicating that offshore participants were driving the market challenge of the BoJ in June, widening into the June BoJ decision, before narrowing as offshore participants pared their bets re: BoJ YCC capitulation

Fig. 3: LCH/JSCC 10- to 40-Year Swap Spreads (bp)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.