Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

Germany's IFO Business Climate index remained in contractionary territory in April but rose for the third consecutive month to 89.4, higher than consensus (88.8) and March's value (87.9, revised from 87.8), and the highest since May 2023. The data broadly mirrors April's flash PMIs, with the uptick driven by the services and construction sectors.

- Both the current assessment (88.9 vs 88.7 cons; 88.1 prior) and expectations (89.9 vs 88.9 cons; 87.5 prior) readings came in above analyst median estimates.

- The improvement was quite broad-based, with the respective diffusion balances of the Business Climate rising in all of the reported sectors. In particular, the services sector (up 2.8p to 3.2, highest since May 2023) and the construction sector (+4.7p to -28.5, highest since July 2023) saw improvement.

- The services sector climate uptick was almost entirely driven by a stronger current assessment (+5.8p to 15.8 in April), while the improvement in the construction sector was based on both a brighter assessment of current conditions and future expectations (+1.3p and +0.9p, respectively). Manufacturing also saw an uptick (+1.4p to -8.5, highest since May 2023) on the back of stronger expectations, though the current assessment balance fell 4.8 points to -8.6, reversing March's gains).

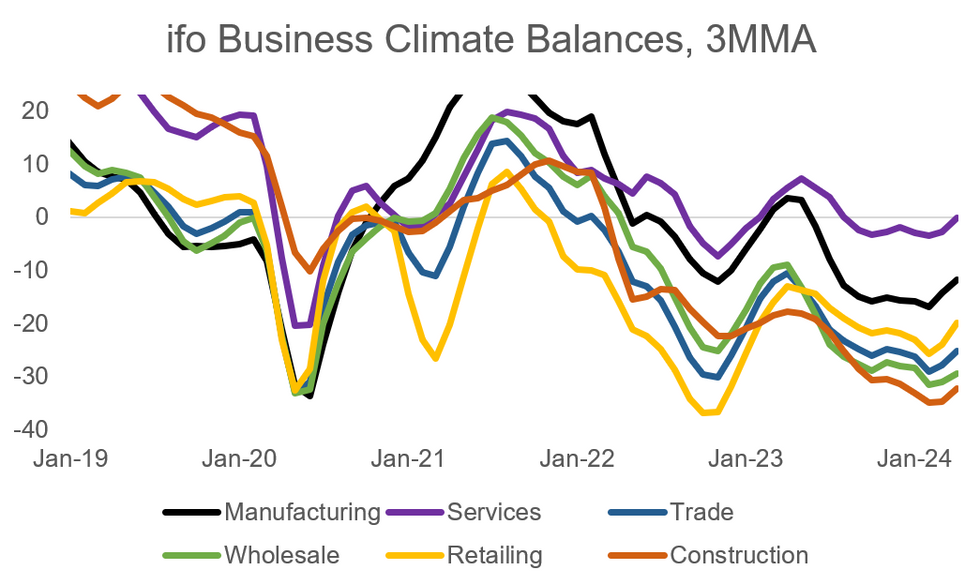

- Looking at the less volatile 3MMA measure, an uptrend seems to be forming, as all sectors printed stronger for the second consecutive month (see chart). The uptrend was most notable in the manufacturing and retailing sectors.

- Overall, the data provide another sign that economic conditions in Germany are stabilising, with surveys mirroring an improvement in "hard" data (including industrial production and services sector turnover). That said, as we outlined earlier this month in our Germany Macro Signal publication (PDF link), other data is weaker and keeps the overall picture ambiguous: for example, the Bundesbank weekly activity tracker suggests some weakness going into Q2, and 'core' factory orders data continue to print lower.

MNI, IFO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok