Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY FUTURES

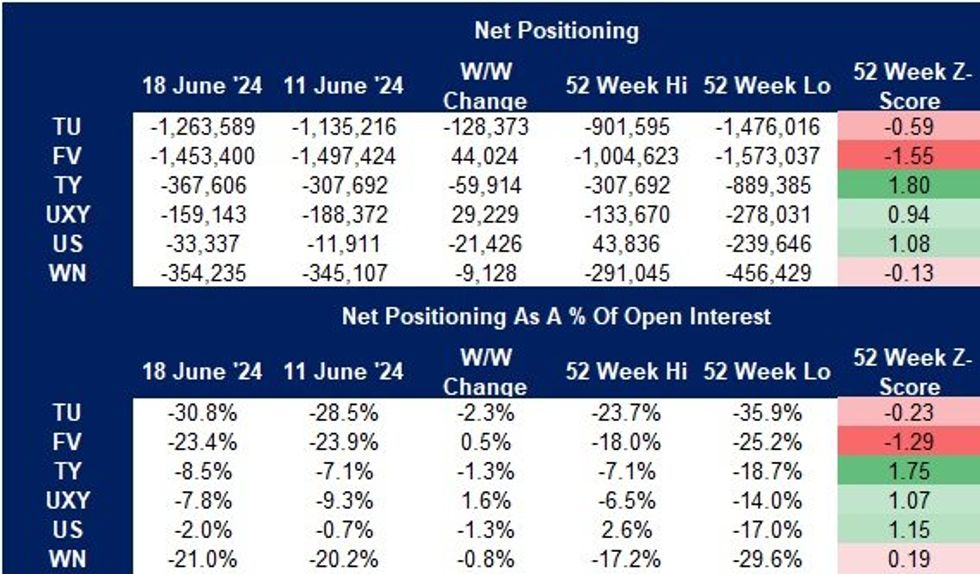

The latest CFTC CoT report (covering the period through Jun 18) showed hedge funds extending already record net short positioning in TU futures, despite a dovish move in FOMC-dated OIS pricing over the survey period

- Conversely, the same cohort’s prior net short position in SOFR futures vanished, as they flipped back to net long positioning.

- Softer-than-expected CPI & PPI readings likely drove the move in their SOFR positioning, providing the major inputs for the dovish adjustment in Fed pricing.

- The survey period also captured the latest FOMC decision, as well as the onset of the French political uncertainty.

- Asset managers extended their overall net long duration position, although trimmed net longs in FV & UXY futures.

- Overall, the report showed a mix of non-commercials extending some existing net shorts (TU, TY, US & WN) and trimming some existing net shorts (FV & UXY).

- CFTC CoT positioning measures will be skewed by basis trades.

Source: MNI - Market News/CFTC/Bloomberg

Source: MNI - Market News/CFTC/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok