Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

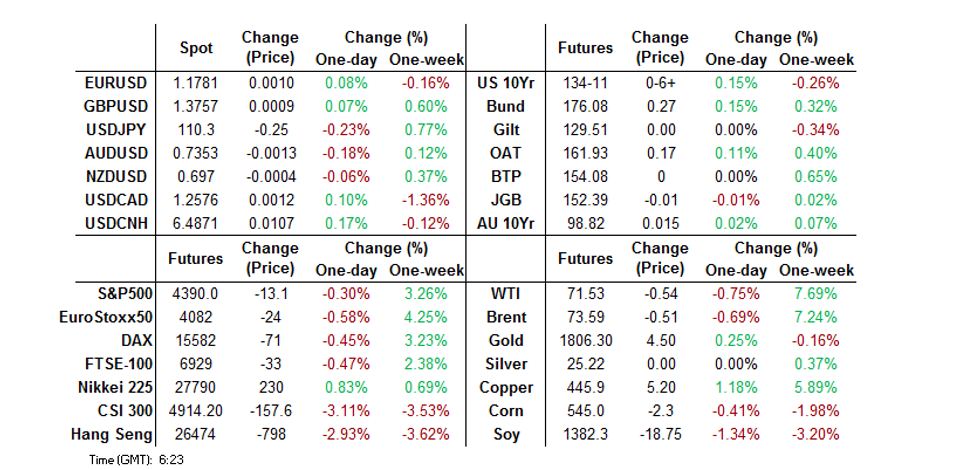

- Chinese & Hong Kong equities struggle, with Chinese regulatory scrutiny and no signs of movement evident at the onset of the latest round of senior level Sino-U.S. talks weighing.

- USD mixed amongst G10 FX.

- U.S. fiscal matters, the Sino-U.S. dialogue and an address from BoE's Vlieghe will likely headline matters on Monday.

BOND SUMMARY: Core FI Generally Bid In Asia

A defensive start to the week for Chinese & Hong Kong equity indices weighed on broader risk appetite, with fears of increased regulatory burden/scrutiny from the Chinese authorities evident in the wake of the crackdown on the education sector, while deeper scrutiny surrounding broader internet based activities also became apparent. This has allowed the U.S. Tsy space to firm, with T-Notes +0-06+ at 134-11, on a mere 68K lots of volume on the day, while cash Tsys print 0.5-2.0bp richer across the curve, as 10s outperform. The opening salvos at the latest meeting between senior U.S. & Chinese officials weren't particularly warm (as was foretold). New home sales & Dallas Fed m'fing activity data headline the local docket during NY hours on Monday, although participants are clearly focused on the upcoming FOMC decision (Wednesday) and advance Q2 GDP reading (Thursday). 2-Year Tsy supply is also due on Monday.

- The latest bid in the U.S. Tsy space aided some very modest richening in areas of the cash JGB curve, with super-long paper perhaps limited by the proximity to tomorrow's 40-Year JGB supply. That leaves the major benchmarks across the cash JGB curve little changed to 0.5bp firmer on the day after the elongated Tokyo weekend. Futures last -2 after unwinding some of the losses witnessed in the final overnight session of last week during morning trade.

- Local COVID matters dominated in Australia, with suggestions in the press that NSW is conducting financial modelling for a lockdown in the Greater Sydney area through at least mid-September. There are also some suggestions that the NSW Treasurer will again request a restart of the JobKeeper scheme. The weekend also saw thousands protest the lockdowns across some of the country's major cities. On a more positive note, South Australia is set to exit its lockdown on Wednesday, although some restrictions will remain in place. Finally, Australia has signed an agreement for the purchase of 60mn additional Pfizer-BioNTech COVID vaccination doses, to be delivered in '22, and a further 25mn doses in '23, which would allow the country to conduct a vaccination "booster" scheme if needed. The A$800mn ACGB Nov '31 auction was well received, with the cover ratio jumping (even when we adjust for the downtick in notional amount on offer vs. the prev. auction of the line), while the weighted average yield printed 0.51bp through prevailing mids at the time of supply (per Yieldbroker). The structurally supportive matters we flagged ahead of the auction outweighed any valuation issues. The curve twist flattened a little as a result, with YM -0.5 and XM +1.0.

FOREX: Risk Off Session Sees High Beta Currencies Pressured

A risk off session saw AUD and NZD come under selling pressure, while JPY shook off a sluggish start to gain through the session as the greenback receded.

- AUD/USD is down 18 pips, the local COVID situation continues to weigh, there are reports that the lockdown in Sydney is set to be extended today while NSW chief health officer said there is likely to be a delay in the second Pfizer doses for non-essential workers.

- NZD/USD is down 12 pips. New Zealand's trade deficit widened in June, the 12-month ytd deficit widened to NZD 252m from a revised NZD 41m. Exports rose to NZD 5.95bn while imports rose to NZD 5.69b.

- USD/JPY is down 19 pips hovering around session lows. Data earlier showed Jibun Bank Japan manufacturing PMI fell slightly to 52.4, services dipped to 46.4 which dragged the composite further into contractionary territory at 47.7.

- Offshore yuan is weaker, USD/CNH is up 102 pips. Comments from the meeting of US and Chinese officials have not been encouraging, Sino-US relations are said to face difficulties.

- USD/CAD is up 18 pips, helped higher by slightly lower oil, the pair remains within Friday's range.

FOREX OPTIONS: Expiries for Jul26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1745-55(E667mln), $1.1830(E622mln), $1.1860(E584mln)

- USD/JPY: Y111.50($510mln)

- GBP/USD: $1.3895-00(Gbp561mln)

- AUD/USD: $0.7330-35(A$555mln)

- USD/CAD: C$1.2570-75($542mln), C$1.2690-00($595mln)

USD: “Easy” Gains Behind Us?

While the resilience and YtD rally witnessed in the broader USD (DXY +3.3% YtD and +4.2% from its YtD trough) has caught many off guard (a reminder that the clear consensus at the start of '21 was for a weaker USD), most, if not all, of the "easy" gains may be in the rear-view mirror for the greenback.

- The aggregate net USD short held within the speculative community since the early part of '20 has unwound, per the latest weekly CFTC CoT report covering the week ending 20 July, if we measure the USD-equivalent value of the futures contracts covered by the report (EUR, GBP, JPY, CAD, AUD, NZD, MXN, BRL & RUB). Levered funds' net positioning has also reverted to net long terms in recent weeks, while asset managers have seen a relatively sharp liquidation of a portion of their net short position, although that investor group's positioning remains comfortably in net short territory (at $36.9bn or 20.6% of open interest). As an aside, asset managers have not been cumulatively net long of USD since '17.

- U.S. economic outperformance has failed to materialise in recent weeks (at least vs. expectations, as evidenced by the Citi U.S. economic surprise index's lack of momentum in moving away from 0), with the fate of the Biden administration's fiscal spending agenda becoming evermore important re: the near-term economic health of the U.S.

- Looking ahead, the key domestic points of interest for the USD over the next month or so include the latest FOMC decision (Wednesday 28 July), U.S. Q2 advance GDP reading (Thursday 29 July), June's labour market report (Friday 6 August) & the Fed's annual Jackson Hole Symposium (Thursday 26 - Saturday 28 August).

- From a technical perspective, the DXY hasn't looked back since breaching its 200-DMA in June, and is close to registering a golden cross formation (whereby the 50-DMA moves above the 200-DMA). Still, the YtD high (93.437) represents the next major target for DXY bulls.

Fig. 1: DXY Index

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

ASIA FX: Mostly Lower, Ringgit Bucks The Trend

A risk off session saw most Asia EM currencies decline, even as DXY also sustained losses.

- CNH: Offshore yuan is weaker, USD/CNH is up 102 pips. Comments from the meeting of US and Chinese officials have not been encouraging, Sino-US relations are said to face difficulties.

- SGD: Singapore dollar is flat, USD/CNH has hovered around neutral levels all session. Industrial production data is due later today.

- TWD: Taiwan dollar is weaker, there were reports n the Commercial Times that the Taiwanese cabinet will propose a 2%-3% increase in spending to at a meeting tomorrow

- KRW: Won declined, South Korea reported 1,318 coronavirus cases in the past 24 hours, down due to fewer tests over the weekend, but infections outside the capital area continued to pile up, triggering toughened restrictions.

- MYR: Ringgit strengthened, markets focus on the first sitting of parliament this year. PM Muhyiddin is expected to face tough questions over his governments handling of the pandemic.

- IDR: Rupiah is flat, clawing back early losses. Indonesia will extend its tightest virus restrictions for another week until Aug. 2 as cases remain elevated.

- PHP: Peso is slightly lower, giving back early gains. Markets await the annual address from President Duterte where he is expected to push for pandemic recovery measures.

- THB: Markets in Thailand remain closed for Asarnha Bucha day.

ASIA RATES: Yields Mostly Lower Amid Negative Sentiment

- INDIA: Yields lower in early trade, recovering from a sell off on Friday. Bonds could come under pressure today, suffering from a hangover of a weak auction on Friday. Indian bonds fell on Friday after a disappointing debt sale, primary dealers were left to rescue the 6.10% 2031 sale taking INR 111bn of the INR 140bn on offer. The weakness at auction was surprising given that this is a new 10-year line.

- SOUTH KOREA: Futures recovered early losses to move into positive territory. • There were reports in Yonhap over the weekend that South Korea is planning to issue up to $1.5bn worth of overseas bonds during the second half of the year to capitalize on favorable funding conditions. According to the reports, the finance ministry has recently completed the process to pick a lead manager for the planned debt sale. Last week Fitch affirmed South Korea at AA- with a stable outlook. Elsewhere the BoK has announced plans to stop issuance of 182-day monetary stabilisation bonds (MSB's) to improve the efficiency of OMOs.

- CHINA: Futures in China are higher. Comments from the meeting of US and Chinese officials have not been encouraging, Sino-US relations are said to face difficulties. Vice Foreign Minister Xie told US Deputy Secretary of State Sherman that some Americans seek to depict China as an imagined enemy, but did note that China was willing to reach a deal with the US on an equal footing. There were reports over the weekend that the Biden administration has no immediate plans to impose sanctions on Chinese officials in response to the Microsoft Exchange hack, which should at least help stop relations from deteriorating further. The PBOC matched maturities with injections. Repo rates rose, the 7-day repo rate has risen above the PBOC's rate last at 2.2258%.

- INDONESIA: Yields higher in Indonesia, some curve flattening seen. Indonesia will extend its tightest virus restrictions for another week until Aug. 2 as cases remain elevated despite restrictions having been in place for a month. Cases have jumped back to over 40k per day after declining from peaks of 56k mid-July.

EQUITIES: Broadly Negative, Japan Bucks The Trend After Holiday

Risk sentiment is broadly negative in Asia, markets in China and Hong Kong the laggards with the Hang Seng down over 2.5%, the CSI 300 is down 2.3%. New Oriental Education saw losses of over 40% on reports of increased regulatory burden/scrutiny, while the Hang Seng tech index saw losses of over 5% . In Japan markets are higher, playing catch up after a four day long weekend. Markets in South Korea, Taiwan, New Zealand and Australia are all also lower. In the US future have declined, e-mini Dow Jones leading the way lower with losses of around 0.5%, failing to build on Friday's positive close where indices saw record highs.

GOLD: Back Above $1,800/oz After Showing Through Support

Spot gold last trades a handful of dollars higher on the day, just above $1,805/oz. Friday's brief showing below short-term technical support was reversed as our weighted U.S real yield monitor moved to fresh all-time lows, while caution surrounding regulatory matters in China and a very tepid start to the latest round of senior level Sino-U.S. talks provided support during the first Asia-Pac session of this week.

OIL: Retreats From Closing Highs

Oil is slightly lower in Asia-Pac trade, retreating from intra-day highs seen at the close on Friday. WTI is down $0.37 from settlement levels at $71.70/bbl, Brent is down $0.35 at $73.75/bbl. WTI and Brent crude futures are both holding most of last week's solid gains and the 10% rally from the Monday low, though markets will continue to assess demand worries from the spread of the delta variant. Oil supermajors earnings in the coming week will be closely eyed, with reports from ExxonMobil, ConocoPhillips among others due. Support for WTI is seen at $69.31, the 50-day EMA while Brent support is at $67.44/43 the low from Jul 20 / 76.4% of the May 21 - Jul 6 rally.

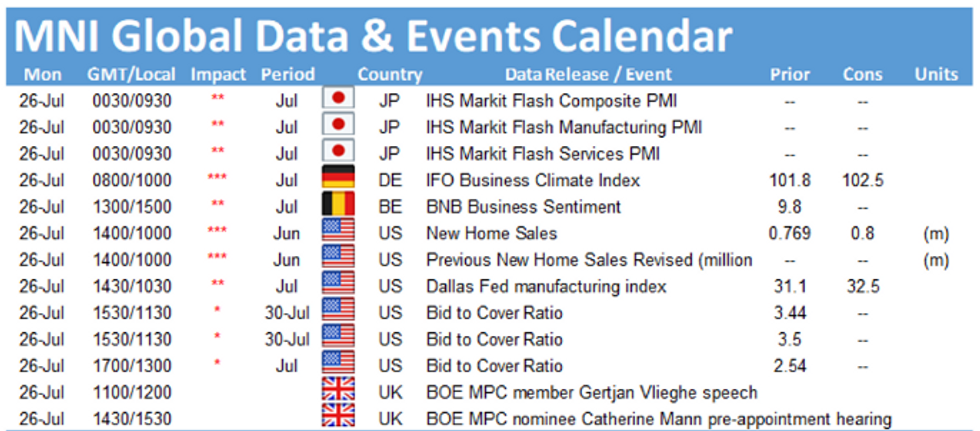

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.