CHINA DATA

Source: MNI - Market News/Bloomberg

- For the PPI, base effects are favorable for a further improvement in y/y momentum over the next few months.

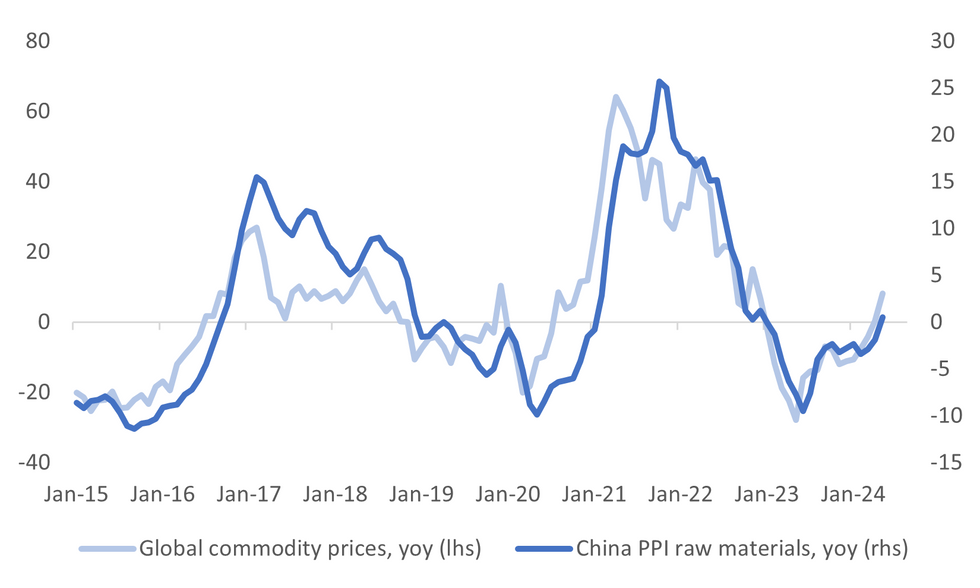

- The global commodity price backdrop is also helping. The second chart below plots the raw materials sub index of the PPI (which ticked up into positive territory, +0.5% y/y), against spot global spot commodity price changes y/y. Mining and manufacturing PPI's were also less negative in y/y terms in May.

- Consumer goods remained negative and close to the April y/y pace.

Fig 2: China PPI Raw Materials & Global Commodity Prices Y/Y

Source: MNI - Market News/Bloomberg

300 words