Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

RUSSIA

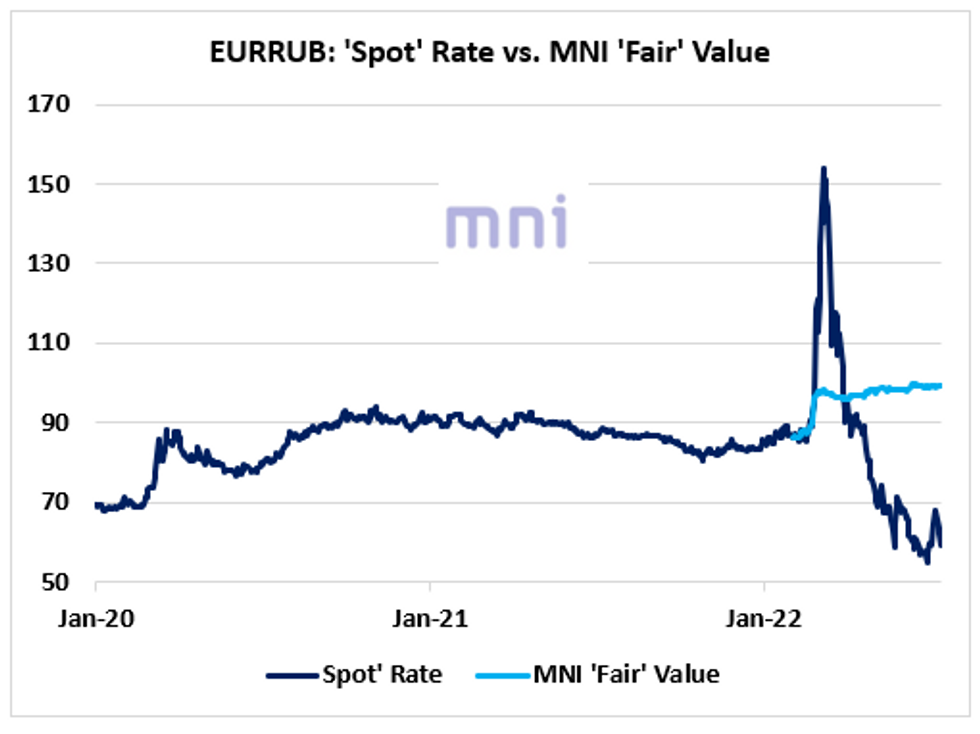

- We previously saw that investors have been questioning in the past few weeks if the Ruble ‘recovery’ was ‘real’ or just an ‘illusion’ as some analysts are expecting a sharp contraction for 2022.

- Economic data recently showed that the current account in Russia surged to a new record high of 70.1bn USD in the second quarter of this year amid surging revenues from energy and commodity exports.

- It is important to note that the significant increase in the trade balance in recent months has been also driven by a collapse of imports, which does not reflect a positive economic sign.

- With Russia ‘defaulting’ on its foreign-currency debt in the end of June, and confidence indicators sitting at extremely low levels, it is difficult to believe that RUB was recently trading at a 7-year low against the Euro and the USD.

- BBG quotes shows that EURRUB is currently trading at around the 60 level, reaching a low at 47.40 earlier this month.

- In addition, the Ruble is not a convertible currency anymore, which can attract arbitraging capital flows, therefore confirming that the current levels are ‘artificial’.

- In this chart, we compute a simple alternative measure of ‘RUB’ using a set of financial and economic variables.

- According to MNI estimations, EURRUB spot rate is more likely to be trading close to the 100 level (than 60), implying that the war and the deterioration in fundamentals have led to a potential 20% depreciation in the Ruble this year.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok