Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

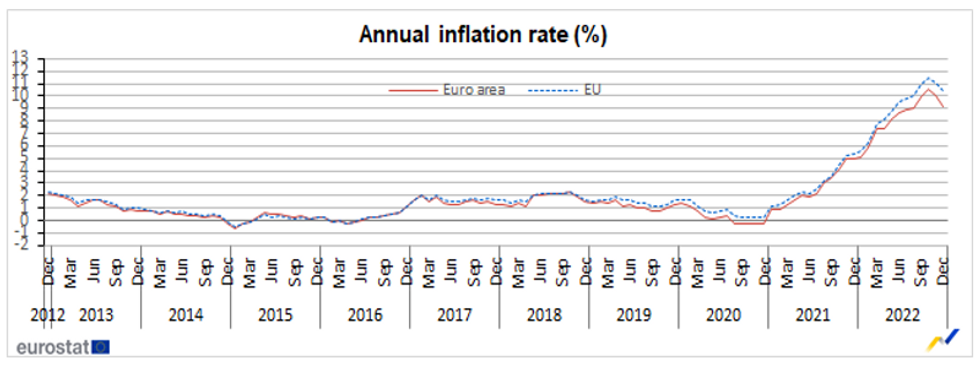

EUROZONE DEC FINAL HICP -0.4% M/M (FLSH -0.3%); NOV -0.1% M/M

EUROZONE DEC FINAL HICP +9.2% Y/Y (= FLSH); NOV % Y/Y

EUROZONE DEC FINAL CORE CPI +0.6% M/M, +5.2% Y/Y; NOV +5.0% Y/Y

- Eurozone final HICP was confirmed slowing by 0.9pp to +9.2% y/y in the final December data. The month-on-month fall in prices was revised 0.1pp lower to -0.4% m/m.

- This confirms a second consecutive month of slowing headline CPI, largely driven by lower energy prices which contributed around 1pp less to the headline print than in November.

- Yet confirmation of the +5.2% y/y record core CPI print implies that prices continue to accelerate in a broad-based manner. Service inflation was up +0.7% m/m alone, increasing 0.2pp to +4.4% y/y. As such, the December data sees continued pressure for the ECB to hike further to get a grip of core price pressures. At the December meeting, President Lagarde stated further 50bp hikes are expected.

- Construction data for November also released this morning saw a -0.8% m/m contraction, remaining a moderate +1.3% above November 2021 levels. The sector remains hampered by weak new orders, as high inflation and rising interest rates weigh further on investment demand.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok