Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

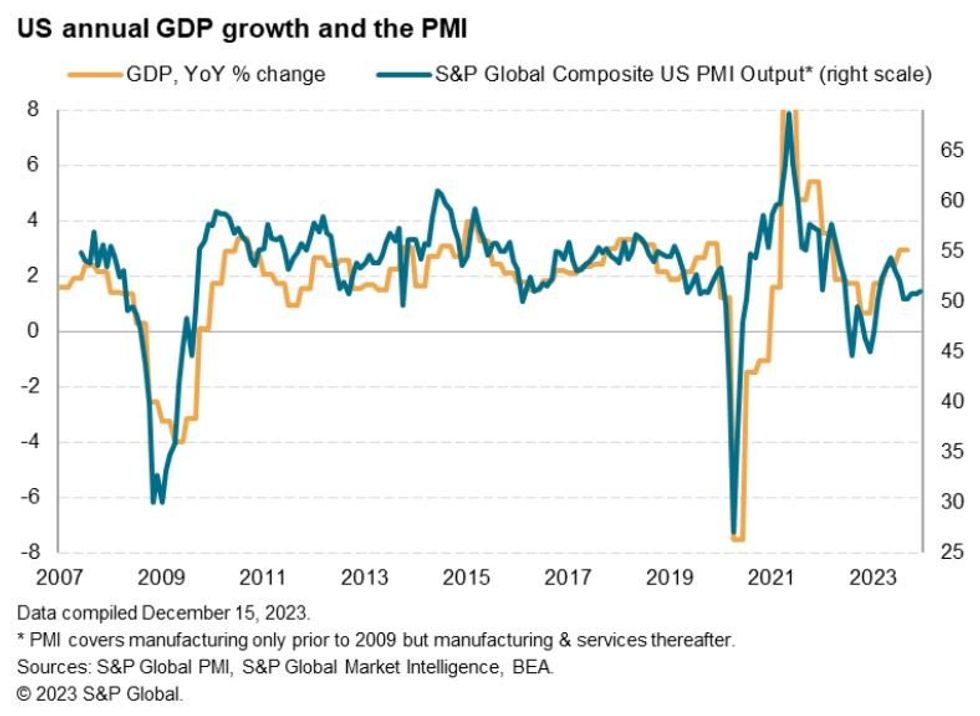

US flash PMI readings for December came in mixed, with manufacturing unexpectedly decelerating sharply to 48.2 (vs 49.5 expected, 49.4 prior), but services unexpectedly accelerating to 51.3 (vs 50.7 expected, 50.8 prior).

- Reflecting the split readings, the Composite index rose to a 5-month high 51.0 (50.5 expected, 50.7 prior), as services rose to a 5-month high but manufacturing fell to a 4-month low.

- From the S&P Global report: "The quicker upturn in output was supported by the sharpest increase in new orders since July. Nonetheless, rates of expansion remained historically subdued as firms continued to highlight challenges stimulating demand. Growth was driven by the service sector, as manufacturers registered a further downturn in new orders and a renewed drop in production."

- Indeed, services sectors saw the joint-highest rise in new business in 6 months ("looser financial conditions" were noted as a factor), though manufacturers saw a quicker drop in new orders.

- The release notes input prices rose to a 3-month high, but a softer prices charged reading vs November.

- There was a "renewed upturn in hiring" with a 3-month high in employment, focused on the service sector, with manufacturers shedding jobs for a 3rd straight month.

- Export orders were subdued for both manufacturers and service providers.

- Overall the report suggests "weak GDP growth in the fourth quarter", with the selling prices index remaining "sticky but at a level which is indicative of CPI running only modestly above 2%.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok