Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

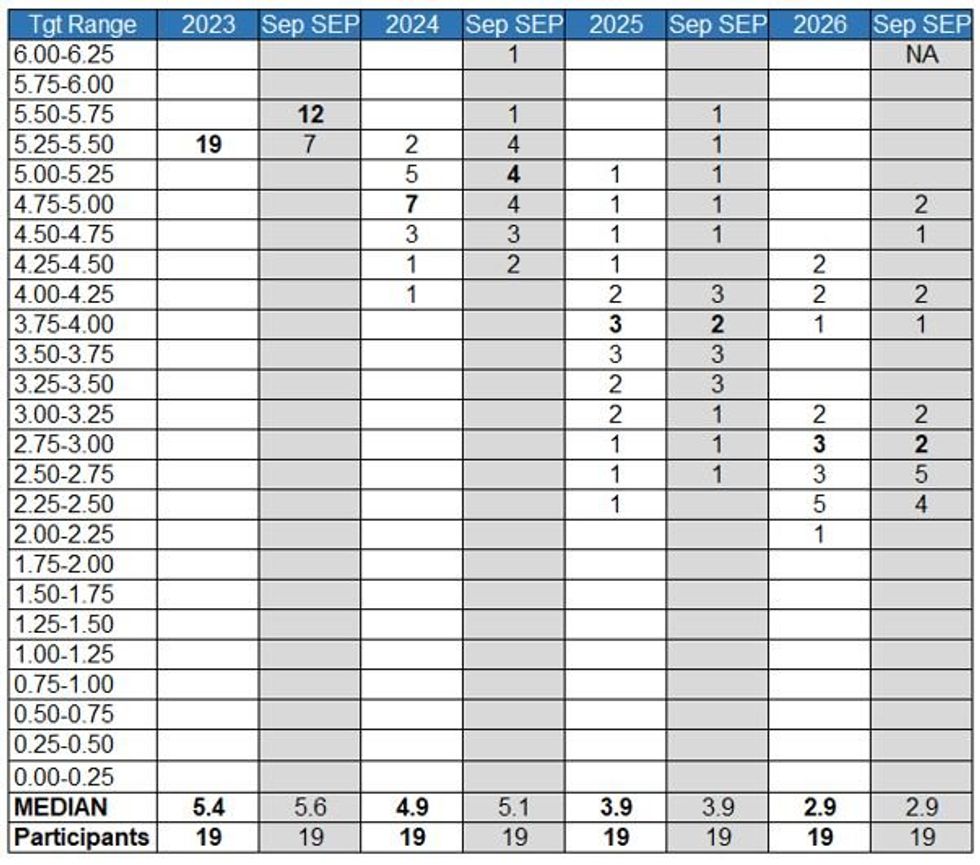

In general, MNI's Markets Team expects December's Dot Plot to push at least slightly against market expectations for substantial cuts next year, with a few members seeing just one or no cuts. (Link to September SEP)

- 2024: The FOMC’s 2024 Fed funds median will be the most closely-scrutinized aspect of the December meeting projections. It’s widely expected that participants will project cuts from the end-2023 level of 5.25-5.50% (equating to a 5.4% rounded midpoint) next year, with consensus appearing to expect that at least two reductions will be penciled in. That would leave the median at 4.75-5.00% (4.9%). That would represent the same 50bp of cutting that had been seen in the September projections albeit those were from a higher starting point of 5.50-5.75%.

- We also note that in September, 9 of 19 members already saw rates at 4.9% or below – meaning that there is likely very little resistance to a lower median. We think that 50bp is basically the level of signalled cuts that says “we acknowledge market pricing and the downward surprises to incoming inflation data but we retain our softening bias toward the next move being a hike”.

- A 5.1% median (ie 25bp cuts) would be extremely hawkish in this context, and 4.6% (ie 75bp cuts) would only be moderately dovish – particularly if it’s widely supported. The latter is about as close to market pricing that the FOMC will get at this point.

- The distribution could thus be important here, and our Instant Answers look for the number of participants eyeing steady/higher rates by end-2024 (>5.125%), and those who see more cuts than the consensus 50bp to be pencilled in (<4.875%) or more than 75bp (<4.625%).

- In the September projections, at least 13 and as many as 17 of 19 members anticipated rate cuts in 2024, with a range of 4.4% (lowest) to 6.1% (highest). That range is due to shift down to 4.1% to 5.4% in our view – meaning the biggest dove(s) sees 100bp of cuts and the biggest hawk(s) no longer see further hikes.

Source: MNI Expectations For December "Dot Plot" Distribution; Federal Reserve

Source: MNI Expectations For December "Dot Plot" Distribution; Federal Reserve

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok