Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

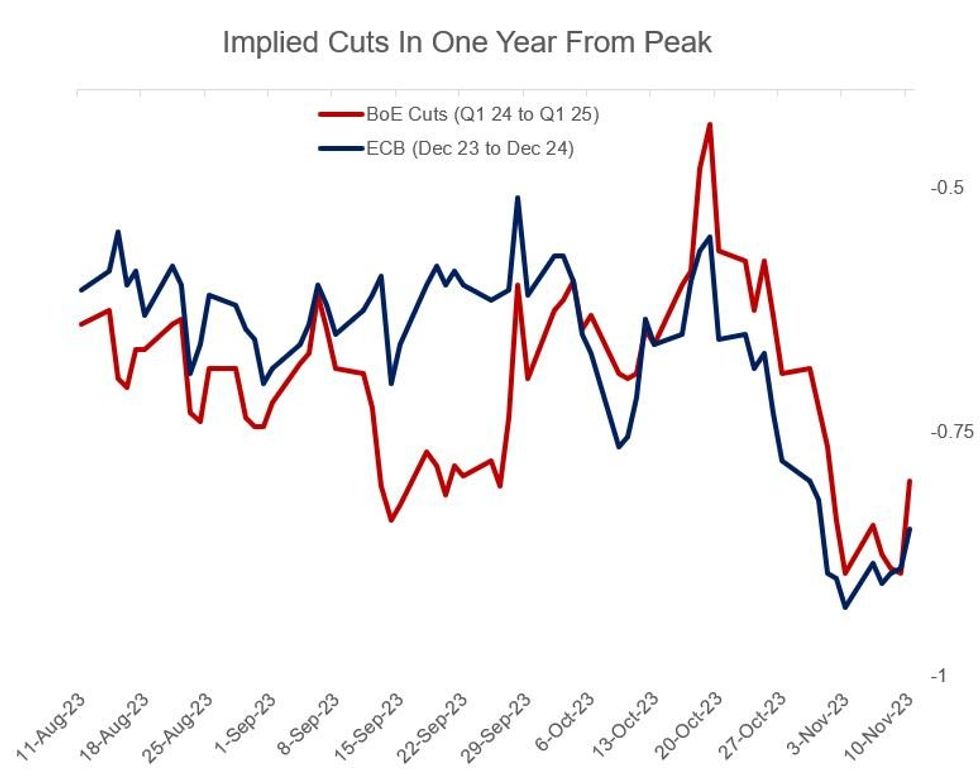

While there remains little change in expected tightening to peak levels for either the BoE (5bp more hikes expected to Feb 2024 peak) or ECB (0bp), cut pricing ends the week relatively unchanged having increased significantly by mid-week. This came after Fed Chair Powell was perceived on Thursday evening to have kept the door to hikes open a bit more than previously seen.

- Implied cuts in the year from peak dropped by 10bp to 79bp - erasing the drop since Nov 3's weak US employment report. That's 12bp less than seen at the week's loosest levels seen Wednesday.

- Cuts seen from peak to end-2024 diminished 8bp to 62bp, equaling the least envisaged cuts since Monday afternoon (and 10bp fewer cuts than seen at the trough on Wednesday).

The pricing out of ECB cuts was less pronounced, but still notable, with implied 2024 reductions pared back by 4bp to 85bp, but still the fewest cuts seen since Nov 1 and vs 95bp briefly seen on Nov 2.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok