Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

Eurozone economic confidence pulled back in February according to the European Commission's monthly Business and Consumer Survey results, with the overall index falling to 95.4 (vs 96.6 expected, 96.1 prior rev.), in what on balance was a relatively soft and disinflationary report versus the previous couple of months.

- Weakness was broad-based. Services sector confidence dropped to 6.0 (9.0 expected, 8.4 prior rev.), with Industrial confidence unexpectedly dipping to -9.5 (-9.2 expected, -9.3 prior rev.). Retail trade sentiment hit a 3-month low and construction a 5-month low.

- The flash Consumer Confidence reading was confirmed at -15.5.

- The readings suggest a slightly more cautionary outlook for Eurozone business confidence than may have been suggested by some national level and PMI readings. We note that the pullback in Services confidence versus the Dec/Jan prints was broad-based, and spread fairly evenly among the big 4 economies.

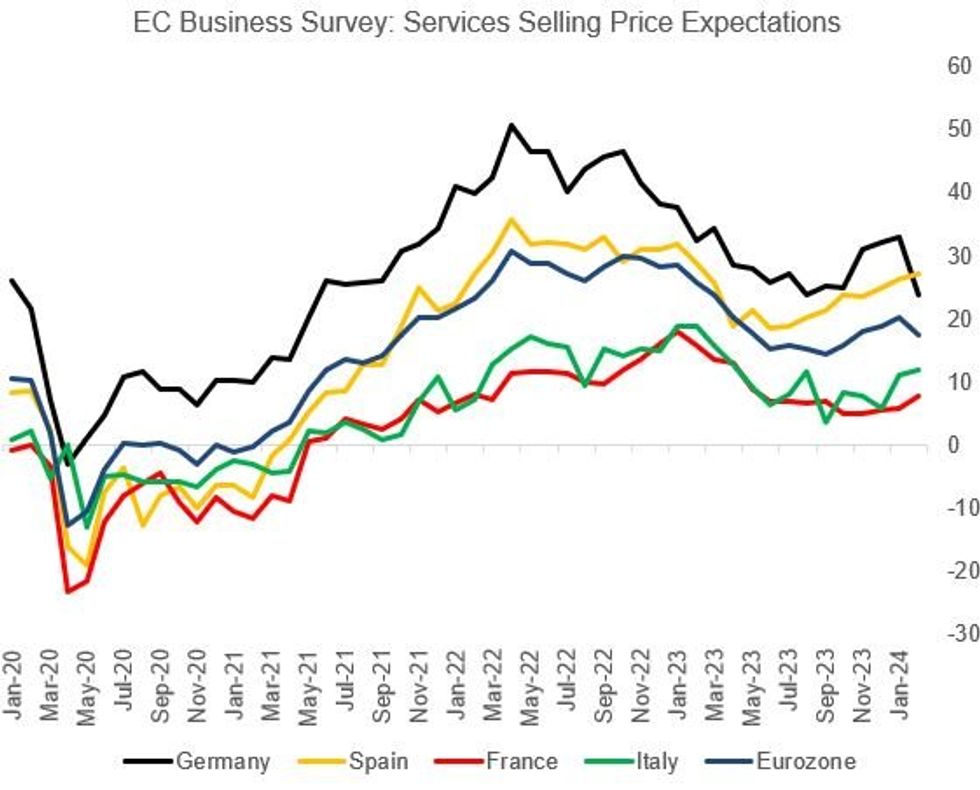

- One potential takeaway from a monetary policy perspective is the dip in services selling price expectations, which at 17.5 marked a 4-month low. This was driven by a sharp drop in German services firms' selling price expectations to 23.8 vs 33.0 prior: a 33-month low, and a sharp reversal from the 10-month high hit in January. Readings out of Spain/France/Italy all ticked higher though, suggesting that the German figure should be eyed somewhat cautiously.

- Industrial sector price expectations meanwhile haven't changed substantially since June, settling at very low levels amid weak activity, largely confirming broader data.

- Any confirmation in service price disinflation (in addition to expectations that industrial goods prices will remain subdued) in hard data would go a long way in shoring up ECB confidence in cutting, but further evidence beyond surveys will be needed.

Source: European Commission, MNI

Source: European Commission, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok