Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

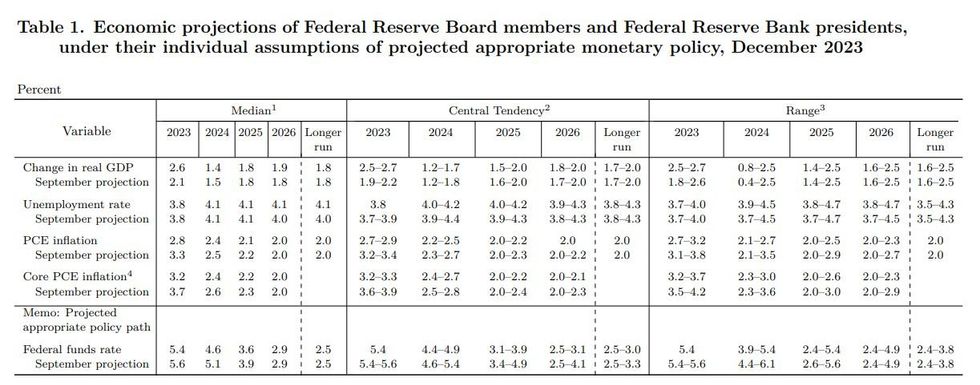

A comparison of December's Summary of Economic Projections to prior September) is below.

- Starting with the Fed funds projections which show cuts as expected, leaning dovish vs consensus but not greatly (4.6% 2024 was a little below the 4.9% most had expected, but some had expected 5.1%). That's a downgrade of 50bp from 5.1% in September's projections (though from a lower starting point of 5.4% in 2023 vs 5.6% projected in September).

- Beyond that 75bp of cuts, 2025 shows 100bp of cuts at 3.6%, down 25bp from 3.9% prior (as expected by most analysts), with 2026 2.9% (unch from prior, not a surprise). Notably the Longer-Run dot stays at 2.5% though some had seen it upgraded.

- The downward inflation revisions for 2023 are more aggressive than expected: core PCE to 3.2% from 3.7% prior. MNI had pencilled in 3.4% but that was before this week's CPI and PPI numbers. It may indeed be the case that the FOMC updated its forecasts after the CPI figure, expect Powell to be asked about this.

- Core to 2.4% in 2024 (vs 2.6% prior) is not a surprise though, with 2025 still showing inflation above-target on both core and headline PCE.

- Growth was revised much higher to 2.6% (from 2.1%) in 2023, around MNI's 2.5% expectation, and as MNI had anticipated, 2024's was revised 0.1pp lower. Somewhat interesting 2026's was revised up to 1.9% from 1.8% but that's fairly meaningless.

- The unemployment forecasts are totally unchanged, in only a modest surprise, apart from the 2026 projection is up 0.1pp and - interestingly - the longer-run unemployment rate is up 0.1pp to 4.1%, which is sure to draw some attention in the press conference.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok