Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

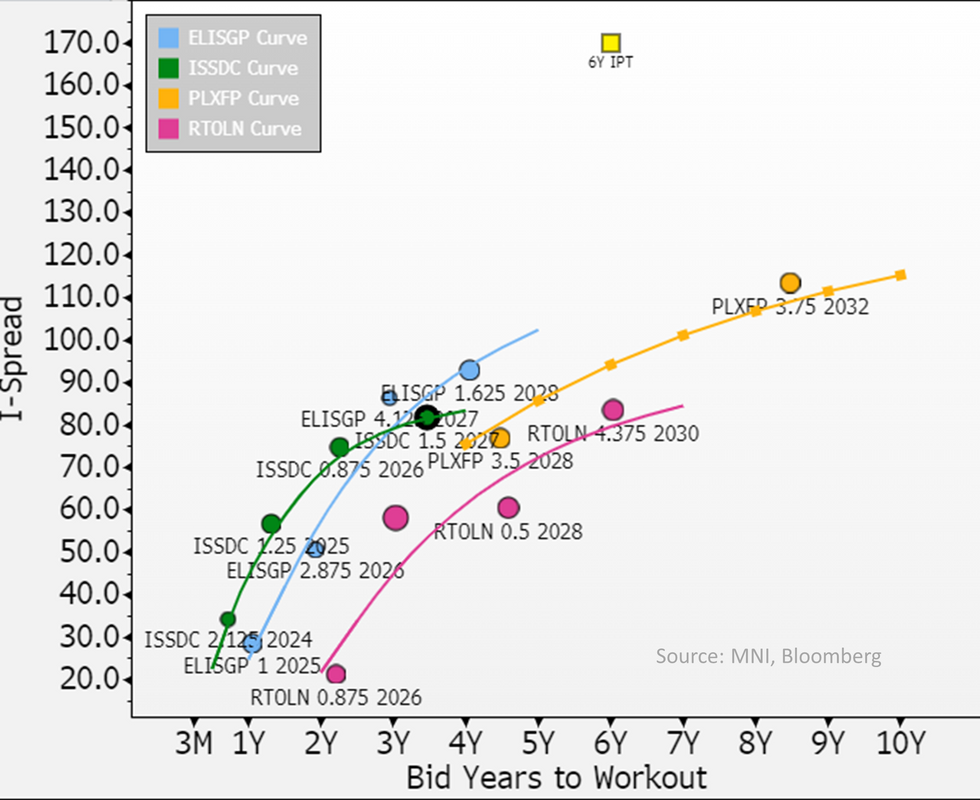

Elis is in the market extending its curve with a new 6yr (IPT +170 – We see FV at 120, i.e. coming wide). Its secondary is +4-6bps.

- As recap Elis is guiding to FCF of €340m in FY24 and continued deleveraging from 2* to 1.8* - it managed to already deleverage from 2.5* to 2* last yr on +€200m EBITDA boost and a €152m decrease in net debt (to €3b).

- De-leveraging will slow this year; of the €340m it’ll use €100m in dividends & remaining majority for the acquisitions with any excess to pay down debt – its relying on EBITDA bump (bbg consensus looking for +8% to €1.6b) for the step down to 1.8* leverage – it didn’t comment on if this was the ceiling going forward but looks like its happy there & should be enough for Moody’s upgrade into IG.

- Moody’s was only looking for debt repayments of around ~€150 million per year & 5% in FCF to debt. Its maturities are spread out and all sub <€500m/singe lines due in coming 5years.

- Somewhat surprising Elis has moved tighter than half-notch higher ISS after S&P’s upgrade to IG in Nov – we don’t see downward rating risk on ISS to justify it trading wider.

- We’re see FV at +120 – it trades wide of consumer staple & auto curves & in line with pharma's VTRS/Bayer. Within the sector itself its spread +20 wide of PLXFP, whose 6yr runs through at +95.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok