Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BONDS

WTI & Brent crude oil futures have moved to fresh YtD highs today, with the well-documented uptick in already heightened geopolitical worry surrounding the Middle East being felt.

- The move comes despite the EIA recently telling MNI that it "expects oil production to be relatively unfazed by (these) tensions," although the Agency does still see prices "rising later this year before receding modestly in 2025."

- European gas futures were initially a little higher but have edged away from best levels to last trade -2.8%.

- On face value, the move higher in crude oil futures should be a headwind for bonds (all else equal), but a demand-side inflationary shock isn’t an indication of healthy economic activity, particularly as the global economy continues to adjust to the post-COVID interest rate environment.

- EUR & USD 5y5y inflation-linked swaps are essentially unchanged on the day (with a very mild bias lower), while EUR 2-Year ZCS show a similar picture.

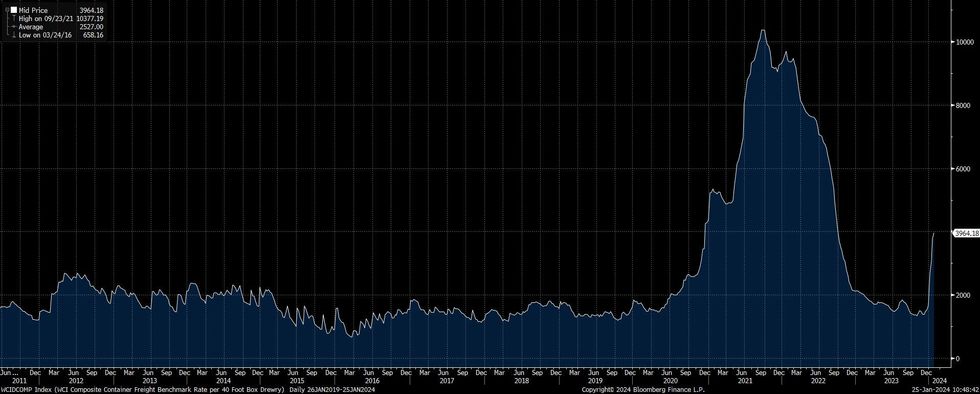

- The Middle East tension-driven move higher in benchmark freight rates remains much shallower than that seen during the COVID-19 pandemic and comes after a moderation back to pre-pandemic norms (as outlined in the below image).

- On this front, HSBC have noted that “even if disruption persists for longer than initially anticipated, is that the world is in a much better position than during the COVID-19 pandemic re: weathering shipping snarls and the same issues with landside logistics (e.g. labour movement restrictions at ports) are not present this time around.”

- When it comes to feedthrough for central banks HSBC notes that "higher shipping costs tend to quickly filter through to producer prices, but the impact on consumer prices can take time to bear out: peaking after around 12 months, according to the IMF.”

- This would suggest that feedthrough into the pricing of the path of policy rates across the major global central banks has been limited thus far (pricing for end of '24 policy rate levels has already pared back aggressively from late '24 dovish extremes).

Fig. 1: WCI Composite Container Freight Benchmark Rate ($/40 Ft Box)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok